Key Highlights:

- The BFSI sector needs robust KYC and AML frameworks to fight financial crimes like identity theft and money laundering.

- KYC verifies customer identity, while AML monitors financial activities to prevent illegal transactions.

- KYC is a one-time process for onboarding; AML is continuous throughout the customer relationship.

- AI and automation streamline KYC by speeding up customer onboarding and reducing errors.

- AML processes use AI to monitor transactions in real-time, quickly spotting suspicious activities.

- Arya AI simplifies compliance with tools like KYC Extraction, Document Fraud Detection, and Deepfake Detection

Every year, an estimated 2 to 5% of the global GDP is lost to money laundering – a staggering 2 trillion US dollars. Know Your Customer (KYC) was first mandated for all banks in the US to prevent fraudulent securities activities and later instated by the EU and other countries as a part of Anti-Money Laundering (AML) initiatives.

KYC finds out who the customers are, and AML monitors their actions. However, KYC onboarding uses confidential information about your customers. Scammers with illegal access to this data and the latest technologies, like deep fakes, can cause massive financial losses, even $35 million for a single case.

Since most fraud activities happen after KYC processes, the BFSI sector also needs robust AML frameworks. Knowing the differences between KYC and AML is crucial as compliance is both a legal obligation and a protection against financial crimes.

What is KYC?

Know Your Customer (KYC) is a regulatory process that financial institutions use to verify the true identity of their customers. The main goals of KYC are to help financial entities prevent identity theft and financial fraud while ensuring compliance with regulations.

KYC typically involves collecting, and analyzing identity documents like passports or Aadhaar cards to confirm customers’ identity, and financial documents like bank statements and credit reports to find the financial capability and risk profile of the customers.

Types of KYC

Financial institutions use different types of KYC for customer identification during the onboarding phase:

- Offline KYC or In-Person Verification (IPV) KYC – where a customer visits in person to submit copies of their ID and address proofs.

- Aadhaar-based eKYC – a remote authentication process in India that uses UIDAI data, Aadhaar OTP, or biometric-based verification like fingerprints.

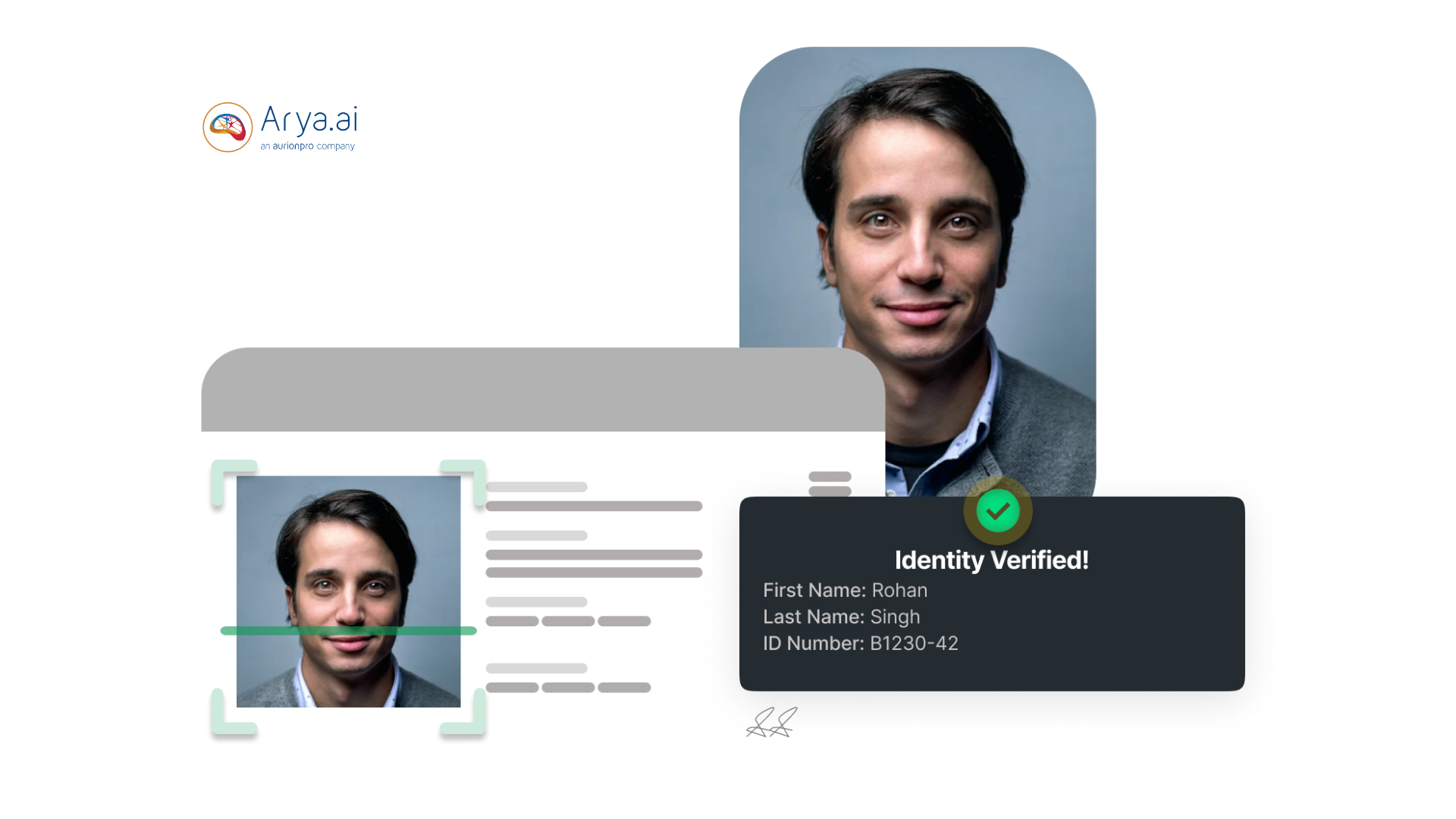

- Digital KYC – automated kyc verification is an online-only option where customers can submit geotagged live photographs (or facial recognition) along with Officially Valid Documents (OVD), which are then verified against geotagged documents.

- Video KYC – a completely remote and paperless verification process with assisted or unassisted video, with manual review by an official staff.

KYC remains a costly proposition for financial institutions, with the average bank spending $60 million a year in Europe. Arya AI’s onboarding tools like KYC Extraction, Document Fraud Detection, and Deepfake Detection are a major relief for BFSI institutions, giving more efficiency for your organization and a better experience for your customers.

What is AML?

Money laundering involves taking illegally collected proceeds and hiding their origins to give every indication of being from a genuine source. Anti-money Laundering (AML) is a collection of laws, regulations and procedures

The main goal of AML frameworks is to make sure that financial institutions do not accidentally allow illegal financial activities and if at all such activities occur, they’re reported to relevant authorities.

In 2022, fines for failure in money laundering defences for global financial institutions surged by 50% from the previous year, totalling over $5 billion. So, financial institutions must invest significantly in AML programs.

Mansi Shah

Mansi Shah

What is the relationship between KYC and AML?

KYC is the first step in a company’s AML program. Once KYC is complete, the data is then used in ongoing AML monitoring.

Together, KYC and AML work to prevent money laundering and other financial crimes, but they have several differences in how they function within a compliance framework.

Differences Between KYC and AML

1. Use and Duration

- KYC is a one-time process for onboarding a new customer and is used for identity verification and risk assessment.

- AML is a continuous process for all financial transactions, monitoring them throughout the customer’s relationship with the institution.

2. Requirements

- KYC requires tools for collecting and verifying customer identities, assessing risk, and ongoing monitoring and updation of customer data.

- AML needs institutions to have broader systems for internal controls, employee training, transaction monitoring, and reporting suspicious activities.

3. Technologies Used

- KYC uses tools like biometrics (facial recognition, fingerprint scanning), Intelligent Document Processing (IDP), and database checks for identity validation

- AML technologies cast a wider net, using AI and Deep Learning, sanction and Politically Exposed Persons (PEP) list screening software, and blockchain analysis tools for tracing illicit funds

4. Working Process

- KYC starts with collecting customer identification documents, followed by verification of their authenticity, and concludes with assessing the customer’s risk before granting access to financial services.

- Every transaction is monitored in AML, and any suspicious activities are reported to authorities. AML systems use algorithms to spot behaviours that don’t match the customer’s usual patterns.

5. Regulatory Framework

- KYC regulations vary by country and are governed by local financial authorities like the Reserve Bank of India (RBI), the USA PATRIOT Act and GDPR in the European Union.

- AML regulations include global standards set by bodies like the Financial Action Task Force (FATF). They are enforced through national laws, like the Prevention of Money Laundering Act (PMLA) in India and the Bank Secrecy Act in the USA.

KYC v/s AML

How AI and Automation Improve KYC and AML?

The rising number of global transactions calls for stricter regulations and makes manual KYC processes obsolete. AI-powered biometrics and automated real-time document verification systems considerably reduce errors and accelerate the KYC automation process. AI improves transaction monitoring by analyzing huge amounts of data in real-time to spot patterns of illegal activity.

Deep learning models and predictive analytics in automated AML solutions help detect complex schemes that manual methods might miss. Automated KYC solutions reduce costs while making compliance smoother. Together, they give your customers a better experience with faster onboarding and enhanced safety.

How Arya AI Helps with KYC and AML

Arya AI helps you stay compliant with KYC and AML rules by using cutting-edge tools that make your job easier. With Document Fraud Detection, you can quickly tell if a document has been tampered with, keeping fraud at bay. KYC Extraction pulls accurate info from Indian KYC documents quickly, and Face Verification makes sure the person is real.

For AML, Deepfake Detection catches fake videos and images, while the Bank Statement Analyser breaks down financial data to help spot any suspicious activity. These tools help you handle compliance faster, safer, and with less effort.

Conclusion

AI and automation are transforming how financial institutions approach KYC and AML compliance, making these processes faster, more accurate, and more secure. With rising threats of fraud and money laundering, using advanced tools like those from Arya AI helps your organization stay ahead in preventing financial crimes.

Contact us to learn more.