The lending industry is undergoing a digital transformation, with AI at its core. Traditionally reliant on manual processes and human judgment, lending is now being redefined by intelligent algorithms. This blog explores how AI in lending is reshaping the industry, from streamlining operations to improving risk assessment and enhancing customer experiences.

We will delve into the specific applications of AI in lending, including credit scoring, fraud detection, and personalized loan offerings. Additionally, we will discuss the challenges and ethical considerations associated with AI in finance. By the end of this blog, you will have a comprehensive understanding of how AI is revolutionizing how we borrow and lend.

AI – The New Face of Lending

The lending industry, once characterized by manual processes and rigid criteria, is undergoing a seismic shift. Artificial Intelligence (AI) is emerging as the catalyst for this transformation, promising to revolutionize how loans are originated, assessed, and managed.

Traditional lending has long been a time-consuming and often opaque process, reliant on paper-based applications, manual credit scoring, and human underwriting. This approach has resulted in lengthy processing times, high rejection rates, and limited access to credit for many individuals and businesses.

However, the landscape is changing rapidly. According to a report by McKinsey, AI has the potential to generate up to $1 trillion in additional annual revenue for the banking industry, including lending, by 2030.

As we delve deeper into this blog, we will explore how AI in lending is reshaping the industry, from improving efficiency and accuracy to enhancing the borrower experience.

Challenges Faced by Traditional Lending

Traditional lending has been a cornerstone of the financial system for centuries, but it is increasingly facing pressure to adapt to the changing landscape. In all these years, traditional lending has heavily relied on paper-based applications, needing manual data entry, verification, and processing. These processes were (and are) time-consuming error-prone, and created massive bottlenecks that led to a negative user experience.

Moreover, it relied heavily on the borrower's creditworthiness, which is a complex task in itself that involves meticulous review of financial documents, credit history, and income verification. Additionally, traditional lending often adheres to strict eligibility criteria based on traditional credit scoring models. These models often overlook crucial factors that could affect a borrower's creditworthiness, such as young age, immigrant status, or those with alternative sources of income.

According to McKinsey & Company, the average loan origination process takes 30 days or more to complete, and lenders lose an estimated $10 billion annually due to fraud and errors.

Traditional lenders face a mounting pile of expenses. Maintaining a physical branch network is costly, and hiring staff to handle paperwork adds up. On top of that, keeping up with the latest technology to prevent fraud is a constant battle.

And finally, let's face it: many traditional lenders are stuck in the past. They're slow to adopt new technologies, leaving customers frustrated with long wait times and complex processes. And forget about personalized service – it's often a one-size-fits-all approach. In today's digital age, customers expect quick, easy, and tailored experiences. Traditional lenders are falling short in meeting these expectations.

This is where AI can come in and completely transform the lending landscape.

AI in Lending: A New Force Reshaping the Banking Industry

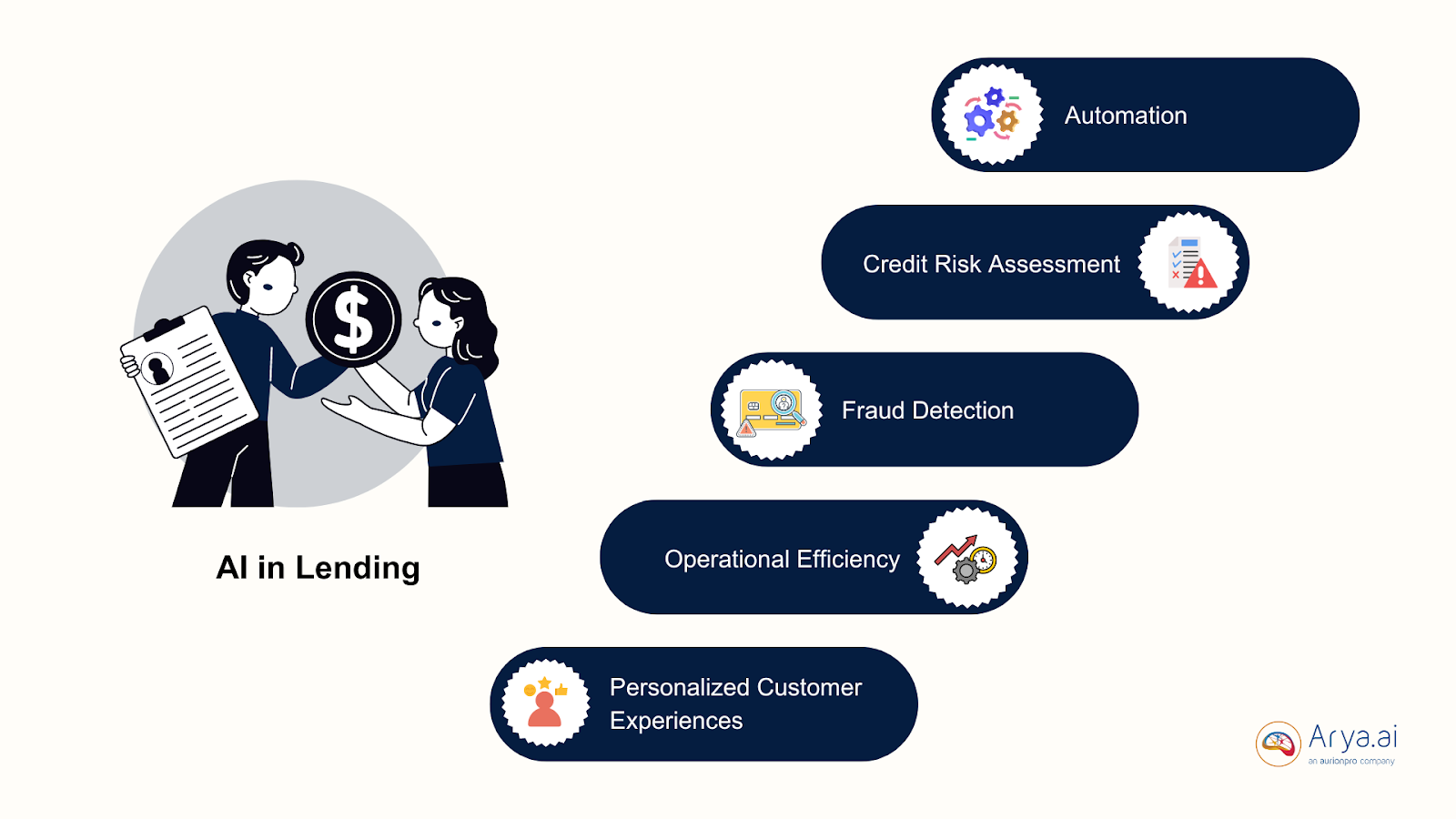

Artificial Intelligence (AI) is reshaping the lending landscape, from how loans are originated to how risks are assessed. At its core, AI in lending involves the application of sophisticated algorithms and machine learning models to analyze vast datasets, identify patterns, and make data-driven decisions. This transformative technology is being harnessed to streamline operations, enhance credit risk assessment, detect fraud, and deliver personalized customer experiences.

- Automation: AI-powered systems can automate routine tasks such as data entry, document classification, document verification, and loan application processing, significantly reducing manual effort and accelerating loan origination.

- Credit Risk Assessment: By analyzing a wide range of data points beyond traditional credit scores, AI in lending can provide a more comprehensive and accurate assessment of a borrower's creditworthiness. This includes factors like alternative data (rent payments, utility bills), social media behaviour, and purchase patterns, easing credit risk assessment processes.

- Fraud Detection: AI's ability to identify anomalies in large datasets makes it a powerful tool in fraud detection. By analyzing transaction patterns, AI algorithms can detect suspicious activities in real time, protecting lenders from financial losses.

- Personalized Customer Experiences: It enables lenders to tailor loan products and services to individual customer needs. By understanding customer behaviour and preferences, lenders can offer customized recommendations and improve customer satisfaction in digital onboarding.

- Operational Efficiency: AI-driven automation and optimization can lead to significant cost reductions and increased efficiency across the lending process, from loan origination to servicing.

How Does AI in Lending Work?

AI in lending is a complex interplay of data, algorithms, and human expertise. Let's break down the process:

Data Collection and Preparation

- Data Gathering: AI in lending systems collect vast amounts of data from various sources, including credit bureaus, financial institutions, public records, and alternative data providers. This data can encompass traditional credit information, income, employment history, social media activity, and purchase patterns.

- Data Cleaning and Preparation: Collected data is cleaned, structured, and transformed into a format suitable for analysis. This involves handling missing values, outliers, and inconsistencies to ensure data quality.

Model Development and Training

- Algorithm Selection: Appropriate machine learning algorithms are chosen based on the specific lending problem, such as decision trees, random forests, or neural networks.

- Model Training: AI models are trained on historical data to identify patterns and correlations between various factors and loan outcomes. This process involves feeding the model with labelled data, where the outcome (loan default or repayment) is known.

Credit Assessment and Decision Making

- Risk Assessment: Trained AI models analyze new loan applications, considering a wide range of factors beyond traditional credit scores. This enables lenders to assess creditworthiness more accurately and identify potential risks.

- Decision Making: Based on the risk assessment, AI in lending can automate loan approval or rejection decisions for low-risk applications, freeing up human underwriters to focus on complex cases.

Continuous Learning and Improvement

- Model Monitoring: AI models are continuously monitored to evaluate their performance and identify areas for improvement.

- Model Retraining: As new data becomes available, models are retrained to adapt to changing market conditions and improve accuracy.

Additional AI Applications in Lending

- Fraud Detection: AI algorithms can analyze transaction patterns to identify suspicious activities and prevent banking fraud.

- Customer Segmentation: AI can help lenders group customers based on similar characteristics, enabling targeted marketing and product offerings.

- Chatbots and Virtual Assistants: AI-powered chatbots can provide instant customer support, answer queries, and guide borrowers through the loan application process.

How AI Can Make a Difference – Real-World Applications

The lending process involves several distinct stages, each presenting opportunities for AI to enhance efficiency and accuracy. Let's explore how AI can be applied at different stages of the lending lifecycle.

1. Loan Application and Origination

The initial stages of loan application and origination are often time-consuming and prone to errors. AI can revolutionize this process:

- Data Extraction: AI-powered Optical Character Recognition (OCR) can swiftly extract essential information from loan applications, such as applicant details, income, and employment history. For instance, OCR can accurately extract data from government-issued IDs like driver's licenses, utility bills, and bank statements, reducing manual data entry errors.

- Eligibility Checks: AI in lending can rapidly assess borrower eligibility by cross-referencing application data with credit bureau reports and other relevant databases. This enables lenders to provide instant pre-approval decisions, enhancing the customer experience.

- Document Verification: AI can authenticate identity documents and verify the authenticity of supporting documents, such as proof of income or address. For example, AI can detect fake documents, forged signatures, altered images, or inconsistencies in document details, mitigating document fraud risks.

2. Credit Underwriting

Credit underwriting is a critical stage in the lending process. AI in lending can significantly improve the accuracy and efficiency of this process:

- Risk Assessment: By analyzing a vast array of data points, including traditional credit scores, alternative data, and behavioral patterns, AI can create a more comprehensive risk profile for borrowers. This enables lenders to identify potential risks accurately and make informed lending decisions.

- Predictive Modeling: AI algorithms can analyze historical loan data to predict the likelihood of default. This information can be used to price loans appropriately, manage loan portfolios effectively, and allocate capital optimally.

- Alternative Data: AI in lending can leverage alternative data sources, such as social media, online shopping behaviour, and mobile phone usage, to supplement traditional credit data. For example, consistent rent payments or utility bill payments can be considered positive indicators of creditworthiness.

3. Loan Approval and Funding

The loan approval and funding stage is crucial for both borrowers and lenders. AI can streamline this process:

- Decision Automation: For low-risk applications that meet predefined criteria, AI in lending can automate the approval process, reducing processing time and improving customer satisfaction. For instance, AI can approve personal loans for borrowers with excellent credit scores and a stable income.

- Fraud Detection: AI document fraud detection systems can analyze application data for anomalies and inconsistencies that may indicate fraudulent activity. For example, AI can detect discrepancies between income information and tax returns or identify patterns associated with fraudulent loan applications.

- Pricing Optimization: AI-powered pricing models can dynamically adjust interest rates based on real-time market conditions, borrower risk profiles, and competitive factors. This enables lenders to maximize profitability while maintaining competitive pricing.

4. Loan Servicing and Collections

Effective loan servicing and collections are essential for maintaining customer relationships and minimizing losses. AI can optimize these processes:

- Customer Service: AI-powered chatbots can provide instant support to customers, answering frequently asked questions and resolving common issues. For example, chatbots can assist with balance inquiries, payment due dates, and address changes.

- Payment Prediction: By analyzing payment history and other relevant data, AI can predict the likelihood of loan delinquency. This allows lenders to proactively reach out to borrowers at risk of default and offer assistance.

- Collections Automation: AI can automate routine collection tasks, such as sending payment reminders, generating collection notices, and scheduling follow-up calls. This frees up human agents to focus on complex cases.

5. Loan Portfolio Management

Effective loan portfolio management is crucial for the overall health of a lending institution. AI in lending can provide valuable insights and support:

- Risk Management: AI risk management modules can continuously monitor loan portfolios for emerging risks, such as economic downturns or changes in borrower behaviour. This enables lenders to take proactive measures to mitigate potential losses.

- Portfolio Optimization: AI can help lenders optimize their loan portfolios by identifying opportunities for growth and diversification. For example, AI can identify customer segments with high-growth potential or low-risk characteristics.

- Customer Segmentation: AI can create detailed customer segments based on various factors, such as demographics, behaviour, and creditworthiness. This enables lenders to offer tailored products and services, improving customer satisfaction and loyalty.

AI for Better Financial Inclusion

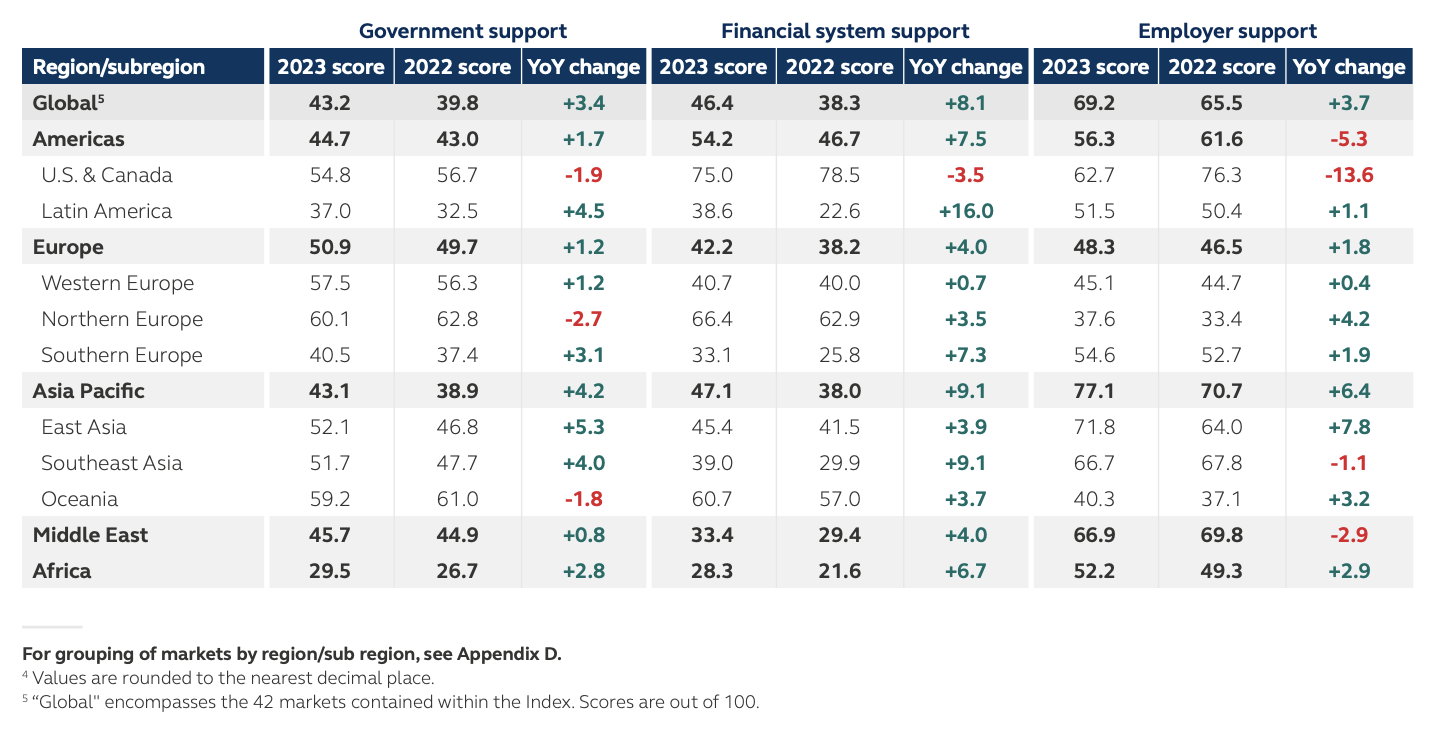

According to a report, the overall global financial inclusion score stood at 41.7 in 2022. In the 2023 index, it increased 5.6 points reaching 47.3

AI has the potential to significantly enhance financial inclusion by addressing the barriers faced by underserved populations. Here’s how:

1. Expanding Access to Credit

- Alternative Data: AI can analyze a wider range of data, including alternative data sources like mobile phone usage, utility bill payments, and social media activity. This enables lenders to assess creditworthiness for individuals with limited or no credit history.

- Microfinance: AI can streamline the process of lending small amounts to underserved populations, making microfinance more accessible and efficient.

2. Reducing Costs

- Operational Efficiency: AI-powered automation can reduce operational costs for lenders, allowing them to offer lower interest rates and fees to borrowers.

- Digital Channels: AI-driven digital platforms can reduce the need for physical branches, making financial services more accessible to people in remote areas.

3. Improving Customer Experience

- Financial Literacy: AI-powered chatbots can provide financial education and guidance to customers, helping them make informed decisions.

- Personalized Services: AI can analyze customer behaviour to offer tailored financial products and services, meeting the specific needs of different segments of the population.

4. Mitigating Risk

- Fraud Prevention: AI can identify fraudulent activities more effectively, protecting both lenders and borrowers from financial losses.

- Credit Risk Assessment: AI-powered credit scoring models can more accurately assess the creditworthiness of individuals, reducing the risk of defaults.

Ritesh Shetty

Ritesh Shetty

5. Enhancing Financial Literacy

- Personalized Financial Advice: AI-powered tools can provide personalized financial advice based on individual circumstances, helping people make informed decisions about saving, investing, and borrowing.

By leveraging AI in lending, financial institutions and banks can create a more inclusive and equitable financial system, empowering individuals and communities to achieve financial well-being.

AI in Lending- Challenges and Considerations

While AI offers immense potential for the lending industry, its implementation comes with several challenges and considerations:

Data Quality and Availability

- Data Bias: Historical data may contain biases, which can be perpetuated by AI models if not addressed carefully.

- Data Privacy: Handling sensitive financial data requires robust security measures to protect customer information.

- Data Quantity and Quality: Sufficient, high-quality data is essential for training accurate AI models.

Model Bias and Fairness

- Algorithmic Bias: AI models can inadvertently perpetuate existing biases if the training data is biased.

- Fair Lending Compliance: Ensuring AI models comply with fair lending regulations is crucial to avoid legal and reputational risks.

Explainability and Transparency

- Black Box Problem: Many AI models, especially deep learning models, are complex and difficult to interpret, raising concerns about transparency and accountability.

- Regulatory Compliance: Some regulations require lenders to explain the rationale behind loan decisions, making explainable AI essential.

Model Risk and Governance

- Model Validation: Regularly testing and validating AI models is crucial to ensure their accuracy and reliability.

- Model Monitoring: Continuous monitoring of AI models is necessary to detect performance degradation and retrain models as needed.

- Model Governance: Establishing clear governance frameworks for AI model development, deployment, and management is essential.

Cybersecurity Risks

- Data Breaches: Protecting sensitive customer data from cyberattacks is paramount.

- Model Tampering: Preventing malicious actors from manipulating AI models is crucial.

Talent Acquisition and Retention

- Skills Gap: Finding and retaining AI talent with domain expertise in finance is challenging.

Regulatory Compliance

- Evolving Regulations: The regulatory landscape for AI in finance is rapidly changing, requiring constant monitoring and adaptation.

Addressing these challenges requires a comprehensive approach that involves data quality management, model development with fairness in mind, transparency efforts, robust security measures, and a strong focus on compliance.

Conclusion

The integration of AI in lending industry marks a pivotal moment in the evolution of finance. By harnessing the power of data and advanced algorithms, lenders can create a more efficient, inclusive, and customer-centric ecosystem. While challenges such as data quality, bias, and regulation exist, the potential benefits far outweigh the obstacles.

As AI continues to mature, we can anticipate even more groundbreaking applications like Arya AI that will redefine the lending landscape. By embracing innovation and addressing the challenges proactively, the lending industry can unlock new opportunities, drive growth, and create lasting value for both lenders and borrowers alike.

The future of lending is undoubtedly bright, and AI will be a key catalyst in shaping that future.