Banks and financial institutions are common targets for fraudsters and attackers seeking financial gain, accessing sensitive information, and engaging in cybercriminal activities.

According to a report, the attempted global fraud transaction volume surged by 92%, and attempted fraud amounts by 146% in 2022 than in the previous year.

Fraudsters and scammers use several tactics, such as phishing, malware infection, and social engineering, to gain unauthorized access to banking customers’ accounts for malicious means.

Financial fraud and scams led banks and financial institutions to lose $485.6 billion in 2023, with payment fraud and credit card fraud generating the highest number of losses, with $386.8 billion and $28.6 billion, respectively.

Given the staggering financial toll of huge financial losses, it's clear that ensuring a robust fraud detection strategy and implementing advanced tools and technologies to mitigate fraud risks is a priority and a necessity for maintaining the trust and credibility of banking institutions.

In this article, we explore the different types of fraud in banks and strategies for mitigating them using advanced software and solutions.

What is Fraud Detection in Banking?

Fraud detection in banking is using a set of tools and technologies to reduce financial fraud risks to institutions and businesses by ensuring secure account access and monitoring user transactions for suspicious activities.

The increasing digitization and use of online transactions have significantly increased financial fraud risks. Thus, given technological advancements and the rise in the financial industry, it is critical to employ robust fraud detection tools and solutions that help prevent and mitigate these risks. Fraud detection in banking is important for lenders to protect their assets, maintain customer trust, and ensure the integrity of financial transactions.

While fraud detection in banking includes identifying and monitoring suspicious activities and anomalies in the user’s transactions and accounts, understanding the different types of banking fraud is essential to easily spot the chances or risks of fraud and take actionable measures to remove them.

A few bank fraud types include-

- Identity theft is where fraudsters gain access to the user’s bank credentials and passwords to conduct huge transactional fraud or access confidential data.

- Account takeover fraud is where the fraudster gains unauthorized access to users’ accounts through malware, spear phishing, or social engineering to extract critical customer data.

- Payment fraud is where the fraudster conducts unauthorized transactions using the user’s cards or account details or even accessing the user’s sensitive financial data.

Check out our blog to learn about financial bank frauds and their risks.

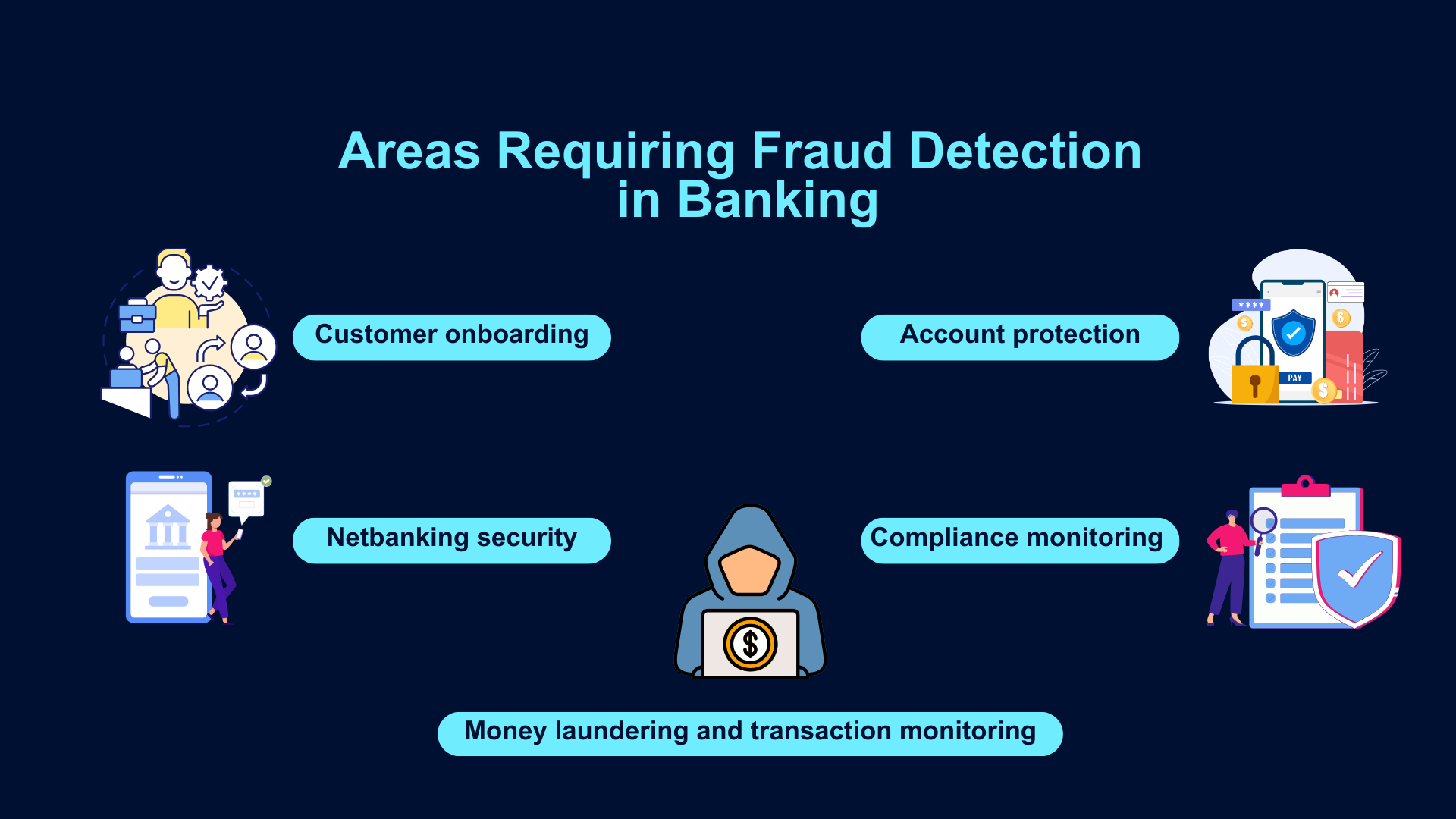

What are the Key Areas Requiring Fraud Detection in Banking?

Banking involves several critical steps and areas that are prone to fraudulent risks and activities. Some of these areas include:

1. Customer Onboarding

Onboarding new customers and opening new accounts always pose a significant banking fraud theft to banks and financial institutions. Ensuring that the new accounts are genuine and legitimate and don’t pose any financial threat is crucial.

This process involves verifying the user’s identity through a credible database and complying with regulatory standards and regulations, which can get challenging. KYC Automation along with robust fraud detection techniques can help enhance customer onboarding process.

2. Net Banking Security

In this highly digitalized and fast-paced world with the boom of net banking and online transactions, implementing robust security measures for online banking platforms is crucial.

While fraudsters continue to develop and use advanced tactics to gain unauthorized access and steal credentials, ensuring encryption during data transmission, secure login processes, and monitoring malware or phishing attempts is crucial to ensure security against potential fraudulent scams.

3. Money Laundering and Transaction Monitoring

Banks and financial institutions often fall victim to scams such as money laundering and illegally acquired funds, which pose challenges to these institutions not only in preventing such activities but also in maintaining their trust and credibility.

Hence, continually monitoring user transactions and investing in a robust transaction monitoring system plays a huge role in detecting suspicious and fraudulent activities or any deviations from normal behavior in the user’s account transactions.

4. Compliance Monitoring

Ensuring compliance with the industry standards and regulatory requirements is of paramount importance to prevent fraud risks and attempts.

Banks and financial institutions must meet compliance with regulations such as Know Your Customer (KYC), Anti-Money Laundering (AML), and Payment Card Industry Data Security Standard (PCI-DSS) to prevent fraud and illegal penalty risks.

5. Account Protection

Account protection is a crucial aspect of fraud detection in banking. It involves implementing various security measures and practices to safeguard customers' bank accounts from unauthorized access and fraudulent activities.

Effective account protection strategies ensure that both personal and financial information is kept secure, thereby maintaining customer trust and confidence.

Fraud Detection Challenges for Banks

Ensuring data privacy while maintaining data security and customer experience is one of the biggest challenges banks face. Here are some of the core challenges for fraud detection in banking:

1. Diverse Sophisticated Fraud

Banks need to monitor and analyze millions of transactions daily to identify instances of fraudulent activities, anomalies, and loopholes each month to prevent fraudulent risks. Manually reviewing each transaction for potential fraud and anomalies gets challenging.

Besides, fraudsters continually devise new and sophisticated methods to conduct fraud and deceive cybersecurity systems, making it difficult for banks to keep up with the increasing security risks, such as phishing, account takeover, and identity theft.

Hence, while automated systems are essential, ensuring and balancing accuracy to reduce risks of false positives is critical to enable secure fraud detection in banking.

2. Increasing Digital Banking Channels

According to a global financial fraud report, digital payment fraud schemes accounted for a total of $485.6 billion in projected losses worldwide.

Digital and online payment platforms have significantly emerged in recent years, creating multiple vulnerabilities and anomalies that fraudsters can exploit for malicious purposes.

Fraudsters try to gain unauthorized access and steal sensitive banking information by leveraging sophisticated techniques, such as malware, phishing, and social engineering. While digital banking has its own merits for banks and their customers, using sophisticated tools and security solutions to prevent digital payment fraud is paramount.

3. Compliance Challenges

Complying with the compliance regulations and guidelines can get challenging for banks, especially when dealing with a large customer dataset and transactions.

Compliance involves regular reviews and audits, structuring and restructuring potential business practices, ensuring high data security, ongoing employee training, and complying with all these regulations can get complex, challenging, and time-consuming.

Failure to comply can result in the banks experiencing legal penalties, damaging the bank’s credibility, customer trust, and reputation.

4. Preventing Credential Theft

Credential theft is one of the most critical banking fraud challenges. Fraudsters steal users' credentials, such as banking details and login information.

Preventing this theft and educating banking employees and customers about the best security practices and password policies is crucial. However, even despite the best attempts and awareness, few banking customers fail to implement the best practices, resulting in fraudulent risks and account takeover attacks.

5. Maintaining Customer Experience

Improving a bank’s security and cybersecurity attempts often impacts customer experience, resulting in loss of customers or another negative impact.

Excessive security protocols, complex authentication procedures, longer onboarding processes, and frozen accounts often have a detrimental impact on the customer experience, leading to negative customer experience.

Strategies for Fraud Detection in Banking

Implementing robust strategies for fraud detection in banking and taking necessary preventative measures is crucial to minimize risks of unauthorized access, financial fraud, data security, company reputation, and customer trust.

Here are some key strategies for implementing fraud detection solutions in your banking processes:

1. Invest in a Reliable Fraud Detection Solution

Investing in a reliable fraud detection solution is the first key step in detecting and mitigating banking fraud.

Using robust AI Apps, banks can help combat fraud detect false positives, improving the overall infrastructure security and operational efficiency. Thus, with the help of real-time data monitoring, data analytics, trend analysis, and AI algorithms, banks and financial institutions can easily detect fraudulent transactions and banking fraud.

2. Employ Real-time Transaction Monitoring

A comprehensive real-time transaction monitoring system significantly helps detect and battle fraud.

A transaction monitoring system not only helps combat fraud but also helps banks comply with regulatory and compliance standards, such as KYC and AML. Banks and financial institutions must first design a base behavioral profile for their customers to establish a baseline for customers’ normal behavior.

This way, any deviations in the customer’s accounts and transaction patterns from the baseline activity can be determined as suspicious, making it easier for banks to flag such accounts and take suitable actions.

3. Implement Document Verification

Document verification is an excellent way to verify the user’s or customer’s identity during the login or onboarding process, confirming their identity and authenticity and ensuring access is granted to genuine and legitimate users.

By verifying documents, such as passports, government-issued IDs like Aadhar cards, PAN cards, driving licenses, or utility bills, banks can easily check the customer’s details and information against reliable and trustworthy databases—to identify any inconsistencies.

By confirming the user’s identity through reliable documents, banks and financial institutions can easily prevent unauthorized access—preventing risks of fraud and identity thefts.

4. Perform Biometric Verification

A biometric verification process uses face verification and a customer’s unique traits and characteristics, making it ideal for security authentication and fraud prevention.

It uses customers’ unique biometric features, such as fingerprints, retinal scans, iris scans, facial features, etc., to verify user’s identity and grant them access to their accounts.

The biometric banking system had a global market capitalization of $5 billion in 2022, which is expected to skyrocket to $23.6 billion by 2032, growing at a Compound Annual Growth Rate (CAGR) of 17.2%.

This exceptional growth of biometric banking solutions is because biometric systems make it extremely difficult for fraudsters to gain unauthorized access without the unique characteristics possessed by the user, reducing risks of account takeover and fraud risks.

Arya AI provides various biometric solutions to automate your verification workflows.

5. Employ a Multi-layered Security System

A multi-layered security system includes a blend of administrative, technical, and physical controls, ensuring a multi-faceted fraud prevention and detection solution.

At the administrative level, banks can develop stringent policies and procedures, such as limiting access, enforcing solid password policies, and implementing compulsory security awareness and training programs to restrict fraud risks.

At the same time, banks must implement technical controls by installing anti-virus software, firewalls, and anti-malware solutions to prevent fraud. Physical controls, such as restricting user access to specific files and folders, are also essential to preventing unauthorized access and fraud risks.

6. Conduct Regular Review Audits

Regular review audits are key to identifying fraud risks and fraudulent activities, either when dealing with new customers or reviewing customer behavior.

Banks must routinely examine customers' bank accounts, transactional patterns and behavior, financial dealings, and internal control systems to determine the presence of loopholes or anomalies or unauthorized and unusual transactions that might indicate fraudulent behavior.

Thus, with regular reviews and audits, banks can ensure early anomaly detection, preventing small issues from escalating to larger fraud. Moreover, it also helps ensure compliance, promote a culture of accountability and transparency, and improve operational efficiency.

7. Lookout for Internal Fraud

Sometimes, threats can come from within, and hence, it is crucial to look out for internal fraud and keep an eye on banking employees with unnecessary access.

It’s crucial to monitor employees and restrict their access from specific locations. Whether accidentally or intentionally, internal fraudsters can expose sensitive and confidential information, such as customer’s passwords, for financial gains.

Keeping an eye on excessive money transfers or funds, processing transactions outside normal working hours, or transferring funds from customers to employees' personal or salary accounts is crucial to identifying and preventing internal financial fraud risks.

8. Provide Regular Fraud Awareness Training and Education

Lastly, educating employees about the evolving cybersecurity threats and ways to look out for potential fraud is crucial to minimizing fraud risks and saving the company's reputation. Fraudsters often target banking employees with social engineering or phishing tactics, luring them to click on malicious links or infect their devices with malware.

Hence, spreading awareness, conducting training sessions for employees regarding fraud detection and mitigation, and following the best security practices can help banks protect themselves against significant threats.

Moreover, banks can also provide useful educational resources to their employees with the latest security threats and mitigation strategies. Hence, they stay up-to-date and equipped with reliable tools to fight banking fraud.

How can AI help in Fraud Detection and Prevention?

Artificial Intelligence and Machine Learning play a crucial role in detecting fraud in the banking and financial sector. These technologies significantly streamline data analysis, making it easier to analyze large datasets, detect anomalies, and make quick decisions.

Statistics suggest AI-based fraud detection in banking is expected to reach $68.6 million by 2026.

By analyzing data in real-time, deep learning algorithms reduce the time required for manual data analysis and review, enhancing productivity and accuracy.

Here are the benefits of AI and deep learning in fraud prevention and detection:

- AI and ML-powered systems process large dataset volumes faster and much accurately, making it easier to identify fraudulent behavior and activities and reducing error margins, false positives, and risks of security attacks.

- By analyzing real-time banking transactions, payment methods, app usage, services availed, and other financial activities, AL and ML accelerate fraud detection in banking and block malicious activities.

- ML algorithms self-learn by past experience and historical data to continue to evolve and adapt to the changing fraud patterns and behavior. This helps mitigate and deal with advanced and sophisticated fraud much easier and faster.

- By reducing the risks of false positives, AI and ML algorithms safeguard and enhance customer experience and security. Besides, 34% of banks and financial institutions said they are likely to invest in AI technologies to offer real-time personalized services to their customers—boosting customer experience and retention.

Arya AI for Fraud Detection in Banking and Financial Services

Using AI and deep learning algorithms to detect and prevent fraud in banking is not only the future but a present necessity. This is why we at Arya AI provide robust and sophisticated Apps, which you can easily integrate into your existing systems to minimize fraud risks.

Here are a few Apps we offer:

- Bank statement analyser thoroughly reads through and scans transactions to any bank statement to extract raw data and convert it into a comprehensive and easy-to-interpret report—facilitating anomaly detection and trends identification.

- Signature detection analyzes any given signature image from several documents and forms to verify the user’s signature at any given stage and return a confidence score for each signature to prevent fraud.

- Passive Liveness Detection analyses any given image to predict whether the person in the picture was present and live at the moment of capture or not. This model works as an anti-spoofing technology against presentation attacks.

- Document fraud detection uses AI algorithms and pattern recognition to detect and avoid fraud by analyzing documents, such as passports, IDs, invoices, bank statements, and more, to determine inconsistencies that may indicate fraud.

Conclusion

Implementing cutting-edge tools and technologies, like AI, to prevent and mitigate fraudulent risks is paramount in today’s digital age.

With the rapidly evolving and growing fraudulent and cybersecurity risks, AI fraud detection in banking can help you preserve sensitive banking and customer data, enhance customer experience, prevent financial losses, and maintain a company’s trust and reputation.

So, make sure you opt for Arya AI Apps to strengthen your banking infrastructure’s security and effectively prevent emerging fraud threats and risks.