Banks and financial institutions handle and manage money not just for individuals but also for huge businesses and the government. Hence, to ensure the integrity and security of the revenue and identity of the entities to whom the money belongs, banks need to comply with strict banking regulations and compliance requirements.

Know Your Customer, or KYC is one such compliance regulation, which is a mandatory customer identification and due diligence procedure that understands and monitors customer behavior and tracks their financial activities to detect anomalies or fraud risks.

With the growing customers, data, and sophisticated fraud techniques, manual KYC processes get time-consuming, inefficient, and challenging and also pose security threats.

Statistics suggest that 67% of corporate treasurers are said to restrict or limit the total number of banks they work with due to KYC-related challenges.

Hence, to overcome these issues, banks are actively seeking automated KYC processes to enhance compliance, combat fraud, strengthen security, and ensure customer trust.

In this article, we'll dive deep into understanding the role and importance of automated KYC verification and how it can help banks and financial institutions combat fraud.

What Is Automated KYC Verification?

Automated Know Your Customer (KYC) verification involves using advanced software and technology to authenticate and verify customer's identities and their documents, including passports, government-issued IDs, utility bills, and driving licenses.

It leverages Artificial Intelligence, advanced data analytics, and machine learning algorithms to speed up and ensure secure, accurate, and efficient customer identity verification.

By improving their KYC/AML processes, banks can save at least $12 million each year. Hence, by automating KYC processes, banks can reduce compliance time and costs and ensure secure and accurate results.

Thus, a digital KYC verification system can help banks enhance compliance with regulatory standards, reduce manual interventions, reduce error risks, and accelerate customer onboarding.

How Does Automated KYC Verification Work?

Automated KYC verification processes use Artificial Intelligence and Machine Learning algorithms to streamline verification processes to enhance accuracy and help banks meet compliance standards.

The process involves using enhanced technology and software to process a large volume of data and documents and boost the system's efficiency.

Here's typically how an automated KYC verification works:

- Data collection: Typically, the first step is the data collection from the users, where the users are asked to provide their personal details, including their name, date of birth, address, etc., along with their identity documents, such as driver's license and passports.

- Data extraction: The advanced systems then use the OCR technology to extract data and text from the documents users submit, scanning document images into machine-readable text. Besides, it uses image recognition to verify and ensure the documents' authenticity and detect signs of forgery or tampering, if any to prevent document fraud.

- Document and identity verification: The AI system then cross-checks the extracted data from the user documents against official sources and databases to ensure its authenticity and validity through document fraud detection tools. Moreover, the system also uses facial recognition or liveness detection techniques to ensure that the user is physically present during the verification process.

- Database and watchlist checks: The AI system checks the user's information against several watchlists, sanctions, and Politically Exposed Persons (PEP) lists to identify potential threats. Additionally, it also performs checks on relevant databases and credit bureaus to validate the user's information, assess risks, and confirm compliance regulations.

- Risk and AML assessment: Digital KYC systems involve AML checks to identify red flags and suspicious activities in the user's financial and transactional history. Besides, based on the collected data and checks performed, the system assigns a risk score to each customer to pay more attention to high-risk score customers to perform additional checks and manual reviews for them.

- Ongoing monitoring: After all the checks and assessments, the AI system continuously monitors the customers and user accounts following the user onboarding process. It uses data analysis and machine learning to detect suspicious transactions and ensure regulatory compliance.

- Approval or rejection: Based on the risk assessment and customer verification, the AI system either approves or rejects the user's application for a banking service or opening an account. It may flag the user application for further manual reviews by a compliance officer if needed.

Manual vs. Automated KYC Verification

Manual KYC verification involves human assistance and intervention to validate a customer's identity and collect relevant information. It's a human-centric approach typically conducted by compliance officers or other personnel to verify individuals or businesses through traditional methods.

While automated KYC verification techniques are on the rise, some small firms and companies still use and rely on manual methods.

Here are a few key differences between the two KYC verification approaches-

Challenges Faced By Compliance Managers For KYC verification

The KYC verification process in banking is one of the most complex, demanding, challenging, and regulated procedures, where banks are constantly expected to balance customer's expectations for speed and available services while meeting stringent and ever-evolving compliance standards and regulations.

While meeting KYC requirements in banking is paramount, the traditional and historically manual processes and legacy technologies banks use for verification make it difficult to meet those requirements.

Here are a few challenges compliance managers typically need to face when it comes to handling KYC verification-

1. Operational challenges

Navigating operational demands is one of the most critical challenge compliance managers face, which often includes resource management and ensuring scalability and data accuracy.

- Managing staff and ensuring there are enough trained and skilled personnel to handle the growing KYC checks volume and evolving fraud is challenging but critical.

- Ensuring accurate and up-to-date data and reducing risks of human-prone errors which can lead to incorrect assessments is essential but can get difficult for compliance managers.

- Another challenge is to maintain efficiency with the growing KYC checks volume and manage the volumes without compromising on timelines, accuracy, and security.

2. Regulatory challenges

Failing to comply with local and international standards and regulations can make banks pay hefty fines and face a disrupted reputation. Not only is ensuring KYC processes comply with these regulations challenging, but staying abreast with the ever-evolving and changing regulations across different jurisdictions is also critical for financial institutions.

Besides, correctly interpreting sometimes ambiguous regulatory standards and implementing controls and processes that meet these regulatory requirements is another huge challenge compliance managers face when handling KYC verification.

3. Technological challenges

Legacy manual KYC verification systems slow down the processes while hampering security, customer satisfaction, and compliance needs. Hence, shifting to automated solutions is critical.

However, compliance managers also face the challenges of migrating data from legacy systems to digital KYC platforms without losing or corrupting data and ensuring seamless integration of automated KYC systems with internal systems.

At the same time, ensuring that the integrated automated systems accurately verify customer identities and detect fraud is essential to overcoming technological KYC verification challenges.

4. Customer-related challenges

Ensuring customer satisfaction is paramount in KYC verification processes. 93% of customers will abandon a banking onboarding application process if it takes more than an hour to complete.

Effective communication with customers to collect relevant information and provide a seamless and quicker KYC verification experience is key and a significant challenge for banks and compliance personnel.

Additionally, managing complex customer profiles, for instance, those with high net worth or entities with intricate structures can get challenging without professional training and experience.

Prathiksha Shetty

Prathiksha Shetty

5. Financial and strategic challenges

KYC processes can cost banks an average of $60 million per year.

Balancing the need for robust and streamlined KYC processes and justifying the need to invest in advanced KYC verification technologies while maintaining and staying on par with the budget constraints is challenging but essential for banks.

6. Strategic alignment challenges

While banks successful integrate advanced KYC verification technologies, they sometimes find it difficult to adapt and sail through the operations while ensuring efficiency.

Aligning the KYC processes with the overall business and banking goals and customer service strategies and ensuring the processes are flexible enough to adapt to the changing business goals is critical but challenging for banks and compliance managers.

Thus, compliance managers need to balance and navigate various challenges, including operational demands, regulatory needs, customer expectations, financial restrictions, and technological advancements, to ensure a successful and streamlined KYC verification process.

How To Implement Digital KYC Verification To Fight Fraud and Improve Compliance?

Banks and financial institutions are keen on enhancing their operational efficiency and mitigating fraud risks through automation. Automating KYC processes is a huge step towards improving and facilitating compliance and fighting fraud.

Here are a few crucial steps to implement automated KYC verification systems:

1. Assess your current KYC processes

Assessing your existing KYC processes is the first critical step towards implementing a digital KYC solution.

It’s important to assess and ask yourself the following questions:

- What are the primary challenges involved in the existing manual operations?

- How long does the customer identity verification process take?

- Are you able to efficiently meet the compliance regulations and requirements?

- Are you able to satisfy your customers and provide a quality experience with the current processes?

2. Choose the right automated KYC solution

Once you’ve identified the pain points in the existing processes and assessed them, the next step is to choose the ideal automated KYC solution to address these pain points.

Here are the things you must look into for an ideal automated KYC verification solution:

- Comprehensive identity verification features, such as biometric authentication, document authentication, and facial recognition.

- Ease in adhering to local and international compliance regulations.

- Intuitive and user-friendly interface.

- Real-time monitoring and alerts for suspicious activities.

- Advanced AI and ML capabilities for sophisticated fraud detection.

- Data security and privacy solutions, such as encryption, access controls, and secure cloud storage.

- Seamless integration capabilities with the existing systems.

- Provide comprehensive reports and detailed analytics into KYC processes to help find bottlenecks and make informed decisions.

3. Integrate the automated KYC solution with the existing systems

After choosing the right solution, the next step is to integrate the automated KYC solution with the existing systems, such as:

- API integration: Configure your systems to efficiently interact with the automated KYC provider’s API endpoints and implement secure authentication (OAuth, API keys, etc.) for secure communication.

- CRM integration: Integrate the KYC processes with the Customer Relationship Management (CRM) solution to streamline customer interaction and data management.

- ERP integration: Ensure you integrate your Enterprise Resource Planning (ERP) system with KYC processes to generate compliance and audit reports within ERP systems.

- AML systems: Ensure you integrate Anti-Money Laundering (AML) systems with the KYC processes to better detect and prevent financial fraud.

- Payment gateways: Iterating payment gateways with KYC processes ensures that payment transactions are genuine and compliant by verifying the customer’s identity.

During the system integration process, it’s essential to ensure secure and frictionless data migration to new systems and also ensure that the integration adheres to the necessary data protection regulations, including CCPA and GDPR.

4. Automate identity verification

You can automate your identity verification processes by:

- Using Optical Character Recognition (OCR) technology to scan and verify customer documents automatically.

- Using liveness detection systems to distinguish between a photo or video spoof and a live person.

- Implementing biometric authentication, such as fingerprint scanning, iris recognition, or facial recognition.

- Leveraging cross-verification solutions to verify the extracted information against government databases or other relevant, trusted sources.

Prathiksha Shetty

5. Implement real-time monitoring

Once the automation implementation is done, implementing real-time monitoring and alerts is essential to ensure efficient risk management.

Monitoring customer transactions to detect suspicious activities and automatically generate alerts and flag accounts can help banks quickly and effectively prevent fraud and data breach risks.

6. Ensure system optimization

Continuously monitoring and optimizing the system’s performance is crucial to meet the changing compliance needs or adapt to the evolving cybercriminal environment is crucial.

It’s important to track key performance metrics, such as customer verification time, drop-off rates, error rates, and fraud detection rates, to identify areas for improvement. At the same time, creating a feedback loop that sends the collected data and customer insights to the internal teams is a game-changer for continuously improving the KYC processes.

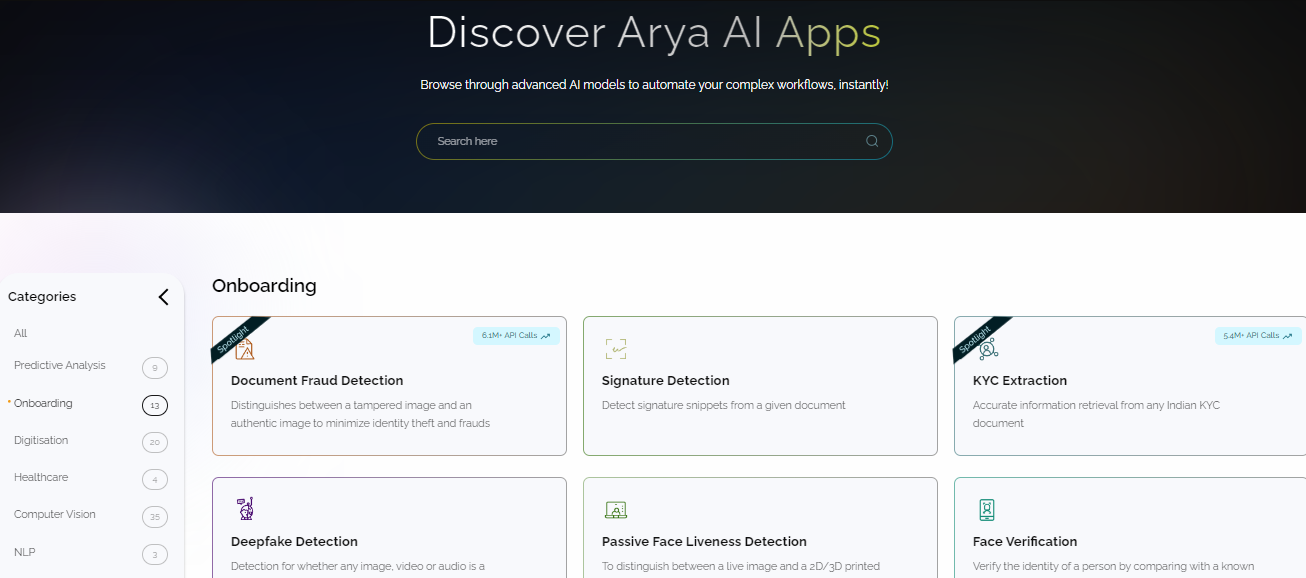

How Arya AI can help you with AI powered Digital Verification?

KYC automation for customer onboarding helps digitally verify identities, reduce manual errors, and accelerate the process while ensuring compliance with regulations. Given the growing importance of fraud prevention and regulatory adherence, Arya AI provides reliable and secure Apps to automate your KYC verification system, enhancing fraud detection and improving compliance.

A few Apps include:

- The KYC extraction App identifies KYC documents such as PAN cards, Voter IDs, and Aadhar cards to retrieve accurate customer information and enable seamless onboarding.

- The CKYC module ensures seamless integration with CERSAI's KYC repository, a centralized repository that maintains records of unique CKYC numbers and customer information. CKYC, with its centralized verification and standardized procedures, strengthens safeguards against identity theft and fraudulent account openings.

- The KYC Corp Extraction App extracts businesses' or corporations' various field information and verifies their details against official government records to ensure seamless, secure, and accurate corporate KYC verification.

- The Passive liveness Detection App analyses any given image to predict whether the person in the picture was present and live at the moment of capture or not. Along with this, the Face Verification App helps recognise and match faces from a variety of sources ensuring authenticity of an individual. This approach safeguards against identity theft and protects your business from fraud.

- With Signature Detection App businesses can authenticate handwritten signatures on documents, ensuring their validity and integrity. This technology helps prevent forgery, enhances document security, and streamlines the verification process.

All our Apps can be clubbed together to create distinct workflows according to your specific requirements. You can easily integrate these App modules within your banks' or financial institutions' existing identity and KYC verification systems to stay ahead of the competition and boost operational productivity.

Conclusion

An automated KYC verification solution solves almost all concerns for banks revolving around meeting compliance, fighting banking fraud, and enhancing customer trust.

It is crucial to choose an automated KYC verification system that seamlessly integrates with your existing system, provides a user-friendly interface, and adapts to changing compliance needs and the fraudulent environment.

Hence, at Arya AI, we offer a comprehensive suite of reliable APIs that are secure, user-friendly, and scalable to meet your KYC needs and enhance customer experience and onboarding experience.

Contact us to learn more.