![KYC Automation with AI [A Complete Guide]](/content/images/size/w960/2024/03/KYC-Automation-with-AI.png)

The current KYC procedures have been resource-intensive, prone to errors, and costly for financial institutions to execute manually. Recognizing the limitations of manual processes amid the escalating risks, institutions increasingly turn to automated KYC solutions.

These solutions offer streamlined verification processes, enhancing efficiency, accuracy, and security while ensuring regulatory compliance.

In this blog, we delve into the significance of KYC automation, exploring its benefits and key components. We also provide insights into how businesses can seamlessly integrate AI and automate KYC operations thus fortifying security measures and elevating the customer experience.

Why is KYC important for your business?

KYC is important for all banks, businesses, and professionals in the “regulated sector,” meaning companies that must comply with Anti-Money Laundering directives in their jurisdictions.

Here are the key factors that make KYC important for businesses:

- Fraud prevention: KYC helps businesses verify customer identities, making it difficult for fraudsters to use fake or stolen passwords. It analyzes customer data and transaction patterns, significantly detecting and preventing suspicious activities and frauds.

- Risk mitigation: KYC allows banks to assess and identify risks associated with each customer based on their financial history, transactional behavior, and background. This allows banks to facilitate ongoing monitoring of customer accounts and implement appropriate measures to mitigate risks associated with high-transaction or high-risk customers.

- Compliance with regulations: KYC enables banks to comply with government legal and regulatory requirements. Many jurisdictions mandate banks and financial institutions to implement KYC as a part of Anti Money Laundering (AML) and Counter-Terrorism Financing (CTF).

- Reduced financial losses: Early detection and prevention of fraud through KYC helps banks reduce financial losses associated with unauthorized access, fraudulent transactions, and legal regulatory penalties—improving the bank’s overall financial stability.

- Better customer insights: KYC operations collect much customer data and information, providing banks and financial institutions valuable insights into their customer base, preferences, and behavior. This allows banks to create tailored solutions and recommendations, enhancing customer experience.

What are the Challenges of current KYC processes?

Traditional KYC systems come with various pitfalls and challenges, and some of them are mentioned below:

- Inadequate database: Inadequate databases lead to inaccurate reports, incomplete data, poor data quality, limited analytical efficiency, and difficulty in auditing, challenging the bank’s ability to adhere to legal and regulatory compliance.

- Time-consuming and error-prone: Manual KYC processes involve collecting and verifying customer data and documents manually—which is highly time-consuming and prone to human errors, delaying customer onboarding and processing transactions.

- Inefficient: Handling data manually is highly inefficient, as it not only takes a lot of time but also requires significant resources, such as personnel and office space, making it difficult for the personnel to focus on other critical tasks that AI can’t handle.

- Data security risks: If not done correctly, handling sensitive and confidential customer information manually increases the risk of unauthorized access, compliance breaches, and data breaches.

- Overhead and onboarding costs: Manual KYC operations are highly resource-intensive, incurring high labor and administrative costs and wasting time and effort, especially when dealing with a large customer database and complex compliance requirements.

- Incompatible systems: Many banks use outdated and incapable legacy systems and processes for customer identification and verification—making it difficult to handle large customer databases, enable scalability, and ensure accurate reports.

- Inconsistent standards: Banks operating in different regions have different regulatory KYC standards, making it difficult to maintain consistency with KYC compliance across different sectors.

- Scalability Issues: A growing customer base makes manual KYC processes incredibly challenging to scale, resulting in scalability bottlenecks and hindering the bank’s expansion.

Why Choose AI-powered KYC Automation for Customer onboarding?

According to a study by Juniper Research, AI implementation by banks and financial institutions in customer identity verification will cut down the time by 30%, reducing the average time spent on a single digital onboarding check from over 11 minutes in 2023 to under 8 minutes by 2028.

This will allow banks to save a whopping $900 million in operational costs.

Here are a few excellent benefits of KYC automation that facilitate bank customer onboarding.

1. Reduced administrative work

Automated KYC processes significantly reduce labor and resources, as AI takes care of most redundant and repetitive tasks, like data entry.

Due to its scalability, KYC automation reduces the demand to hire data entry or manual data review specialists. It allows banks to save labor costs and allow specialists to work on more complex and critical tasks.

However, this doesn’t mean banks must eliminate the human factor of KYC operations. When combined with human intelligence, KYC automation results in much more accuracy and efficiency.

2. Accuracy

Accuracy is one of the primary benefits of KYC automation, as automated systems and processes are less prone to errors, such as misinterpreting documents or silly typos.

This results in banks saving a database of precise, accurate, and reliable customer information—beneficial for banks to maintain a high level of customer data quality and meet regulatory requirements.

3. Enhanced security and fraud prevention

KYC automation processes often include measures that ensure robust data encryption, multi-factor authentication, and secure access controls, which protect customer data from breaches and unauthorized access.

Moreover, since AI-powered KYC operations also ensure real-time monitoring of customer transactions, patterns, and behavior—it makes it easier for banks to detect suspicious or abnormal activities and transactions—reducing the chances of fraudulent breaches and financial crimes.

4. Better customer experience

Automating KYC verification during customer onboarding streamlines customer interactions—resulting in faster onboarding, reduced friction, and quicker access to banking services.

This makes the entire onboarding process user-friendly, enhancing customer experience, increasing customer loyalty and satisfaction, making a first good impression of the bank, and leaving a positive brand image.

5. Regulatory compliance

By ensuring high data accuracy and the ability to adapt to evolving regulatory and compliance requirements, automated KYC solutions help banks meet regulatory needs and avoid legal trouble and penalties.

6. Substantial cost savings

Automated KYC solutions are more cost-efficient for banks than manual KYC processes as they reduce labor costs and the risks of human errors and fines associated with non-compliance.

This allows banks to reduce operational costs and improve their overall financial performance and stability.

Implementing KYC Automation: A Step-by-Step Guide

According to the statistics, only a mere 2% of businesses, including financial institutions, managed to automate 90% of their overall KYC operations. At the same time, 28% of firms still perform 41-60% of KYC operations manually.

This is mainly because of the lack of knowledge regarding taking the right steps towards KYC implementation.

Here is the step-by-step process to implement KYC automation to enhance banking operations and customer onboarding.

1. Conduct a thorough assessment of current processes and compliance requirements.

The first step for banks is to evaluate the existing KYC processes, including manual KYC operations, compliance measures, and technology infrastructure, to identify pain points, areas for improvement, and compliance gaps within the current processes.

Making a list of all the regulatory compliance requirements applicable to the banks and financial institutions, such as Customer Due Diligence (CDD) and Anti-Money Laundering (AML), is critical for effective KYC automation implementation.

2. Determine clear KYC automation goals and objectives.

Once you can identify the gaps, the next step is to list down and determine the goals to achieve with KYC automation. These goals could be enhancing compliance, reducing customer onboarding time, improving customer experience, or improving data accuracy.

At the same time, determining the project's scope and planning the project details, including outlining timelines resource requirements, and achieving key milestones.

Determining the types of customers and transactions the bank needs to cover also helps strategize the project goals effectively.

3. Select a suitable KYC automation vendor.

Once the goals and objectives are ready, the next step is to choose a KYC automation vendor that offers services that meet your KYC automation objectives.

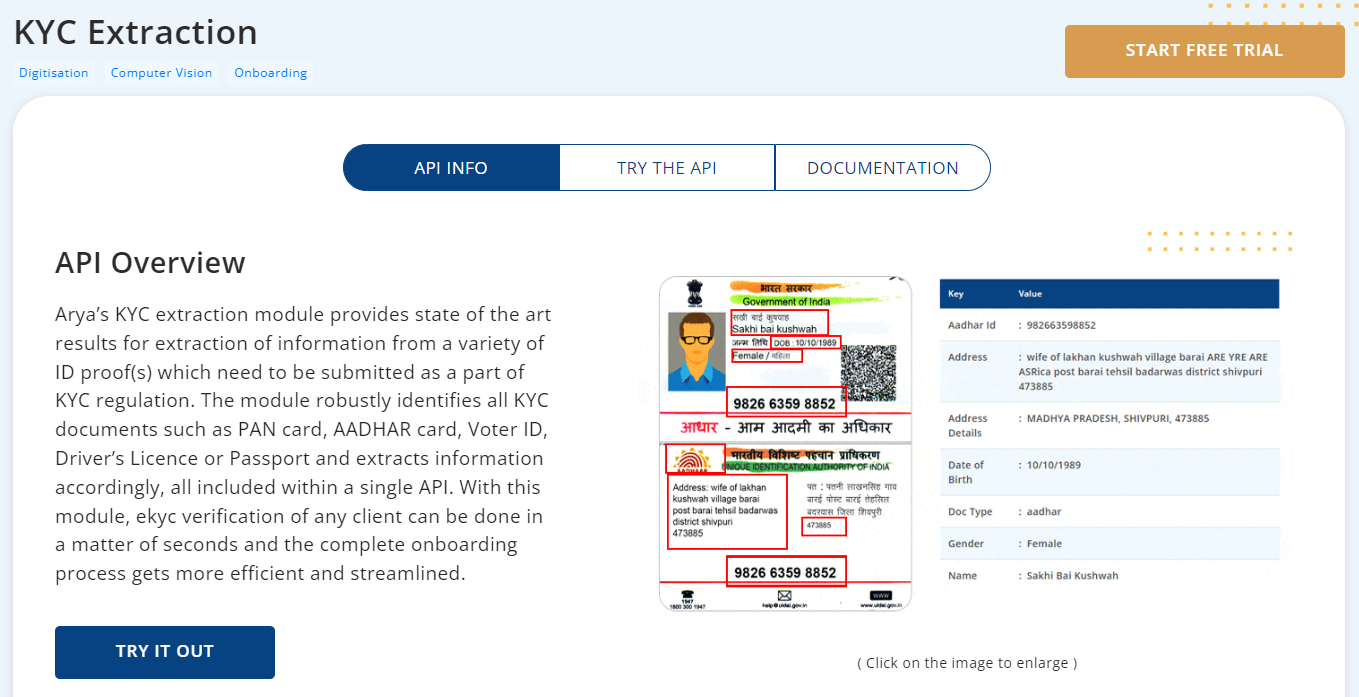

It is crucial to research vendors based on their flexibility, scalability, integration and reporting capabilities, regulatory compliance, user interface, and ongoing support services. Along with this, prioritize vendors who offer comprehensive solutions with KYC extraction, KYC verification, and all necessary APIs conveniently accessible in one place. This streamlines your processes and ensures seamless integration into your operations.

Selecting a KYC automation vendor that best meets your bank’s objectives, requirements, and budget is critical for long-term success.

Read: Top 10 identity verification providers in 2024

4. Data collection and integration

Once the right vendor is selected, it’s time to integrate the existing customer data with the vendor’s KYC automation processes.

Consolidate relevant customer data and information from internal and external sources, such as the customer database, third-party verification services, and identification documents, like passports, utility bills, and driving licenses.

After collecting the data, it’s critical to integrate KYC automated solutions with existing systems, such as risk management platforms and Customer Relationship Management (CRM).

5. Workflow automation implementation

Once the data collection and integration are done, the next step is configuring and streamlining workflows for automated KYC processes, including customer onboarding, risk assessment, identity verification, and ongoing monitoring.

At the same time, automating processes, such as task assigning, escalations, and notifications, is also crucial for a streamlined and efficient KYC workflow.

6. Compliance monitoring and reporting

The next step is configuring real-time monitoring tools and systems to track customer transactions and detect suspicious activities and deviations from customer’s established transaction patterns.

Generating comprehensive reports and audit trails is important to demonstrate legal compliance with regulatory requirements, such as CDD and AML regulations.

At the same time, it automates the filing of regulatory reports, such as Currency Transaction Records (CTR) and Suspicious Activity Reports (SAR), to relevant authorities through regulatory reporting systems and integration.

Moreover, periodic audits and reviews of KYC automation operations are conducted to ensure compliance and effectiveness.

Arya’s AI APP for KYC Automation

Arya's AI KYC APP provides an all-encompassing solution for automating KYC procedures, accelerating the resource-intensive process. By leveraging pre-trained models and deep learning algorithms, technical complexities are eliminated.

Simply plug and play the app into your system without any coding or complicated set-up hassle, and it seamlessly begins operations without extensive technical expertise.

Key features of the Arya KYC API-

- Auto Classification and Verification: Arya's AI KYC app employs advanced algorithms to automatically classify documents and verify the authenticity of the information provided, reducing the need for manual intervention.

- Auto Extraction & Tampering Checks: It has the capability to automatically extract relevant information from documents while simultaneously checking for any signs of tampering or manipulation, ensuring the integrity of the data.

- No-code Set Up: The app offers a no-code setup, making it easy for businesses to implement and integrate into their existing systems without extensive coding or technical expertise.

- Intelligent Deep Learning Algorithms: Arya's AI KYC app utilizes deep learning algorithms, continuously improving its accuracy and efficiency over time as it processes more data and encounters new scenarios.

Key Components of KYC Automation Solutions

When looking for automated KYC solutions, here are the key components banks and businesses must look for:

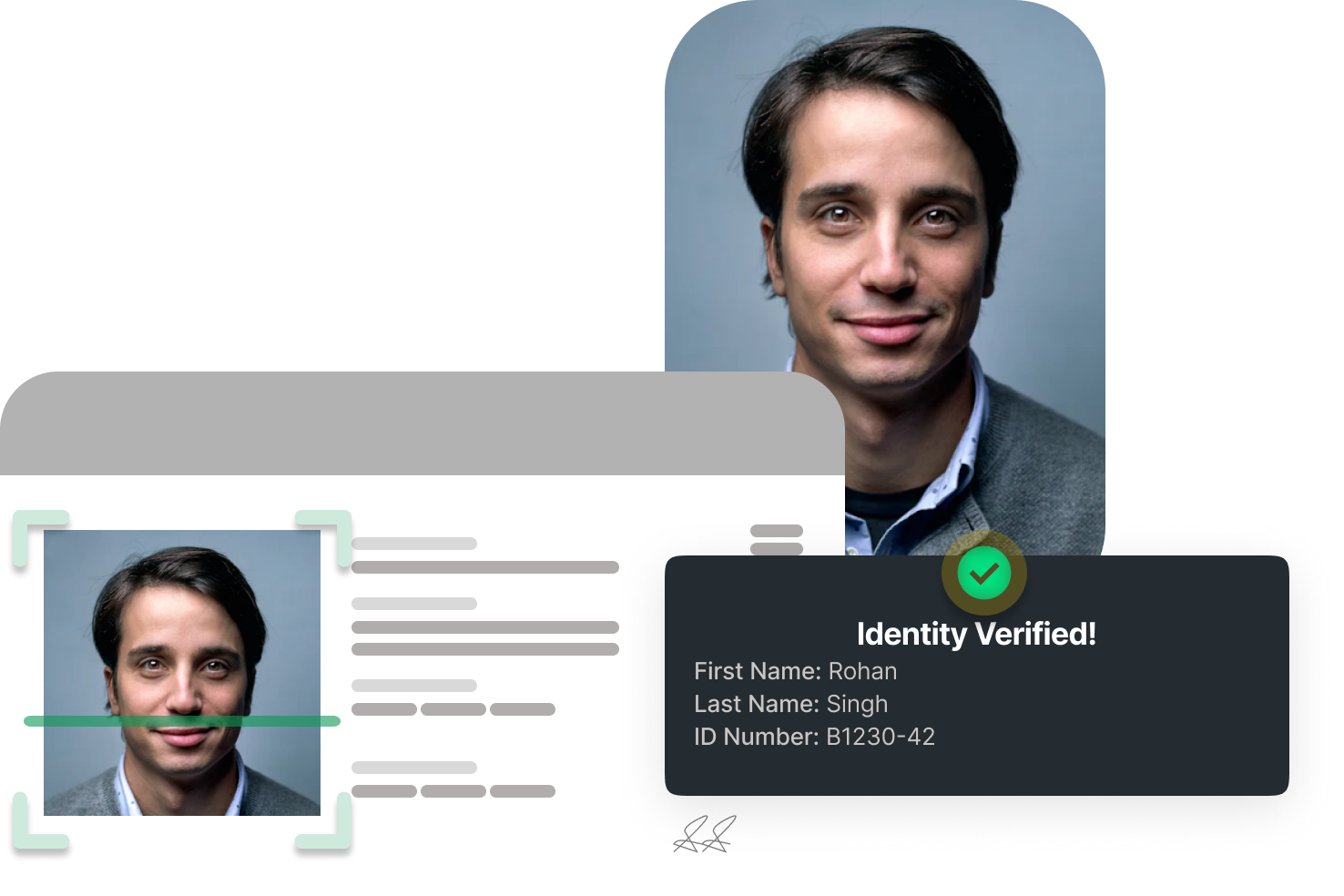

- Identity verification: Customer Information Program (CIP) or identity verification that requires customers to provide their name, address, date of birth, and identification number. Using KYC automation, banks compare these details with the customer’s government-issued IDs to confirm the customer’s identity.

- Data extraction and document verification: This component includes using Optical Character Recognition (OCR) and NLP to extract data from customers’ identity documents, like driving licenses and passports, to detect data forgery or tampering.

- Biometric authentication: This includes implementing biometric authentication methods, such as facial recognition, fingerprints, and voice recognition, for enhanced identity verification.

- Fraud detection: This critical KYC automation component includes utilizing machine learning algorithms to compare customer identification data with historical data to flag inconsistencies and suspicious and fraudulent activities to avoid potential risks.

- Risk scoring and profiling: This includes assessing risks associated with each customer using a risk-scoring module based on their collected data. This helps banks and financial institutions determine the right due diligence needed to segment customers based on their risk profiles and pay more attention to such customer profiles.

- Integration with compliance and regulatory guidelines: This component aligns KYC automation with regulatory guidelines to ensure legal compliance with specific regulations and ensure the KYC processes comply with evolving standards and regulations.

Future Trends in KYC Automation and AI

The constantly evolving cybersecurity threats, technologies, and regulations require banks to address KYC more efficiently and streamlined. Hence, banks must adjust and evolve their KYC processes to surpass the technological trends and risks.

Here’s what the future of KYC automation looks like:

- Added regulations: Fraud and malicious activities will continue evolving and developing with new tactics with their economic downturn and geopolitical wars. Government agencies are more likely to update their regulations to address the current and emerging threats. An example is when the adoption of tools like digital signature software accelerated during the COVID-19 pandemic when it changed the customer due diligence procedures overnight.

- Increased use of AI and ML: AI and ML are set to play pivotal roles in KYC operations, catching money laundering behavior, offering sophisticated solutions for data analysis and behavior recognition, and automating complex tasks like risk assessment and document verification.

- Wider ESG reporting demands: With the growing importance of Environment, Social, and Governance (ESG), banks will need to adapt to efficient ways to ascertain customer’s ESG efforts and ratings to ensure compliance.

- Increased competitiveness: KYC will also provide a competitive advantage to banks and financial institutions, allowing them to strive to implement intelligent solutions and automation and improve customer experience through secure and efficient KYC processes.

Conclusion

KYC automation is essential to helping banks prevent fraud and illegal activities, meet compliance regulations, and enhance customer experience.

Automated and efficient KYC processes streamline customer onboarding—increasing the bank’s reputation and trustworthiness. From advanced data analytics for fraud assessment and prevention to robust identity verification systems, KYC automation improves the bank’s overall efficiency, image, and security.

So, realize the potential benefits of KYC automation and help your financial institution strive for success.