Several types of financial fraud exist, including credit card loan fraud, unauthorized transactions, and cheque fraud. Of all these financial frauds, forged documents or document fraud is one of the most common and growing fraud risks.

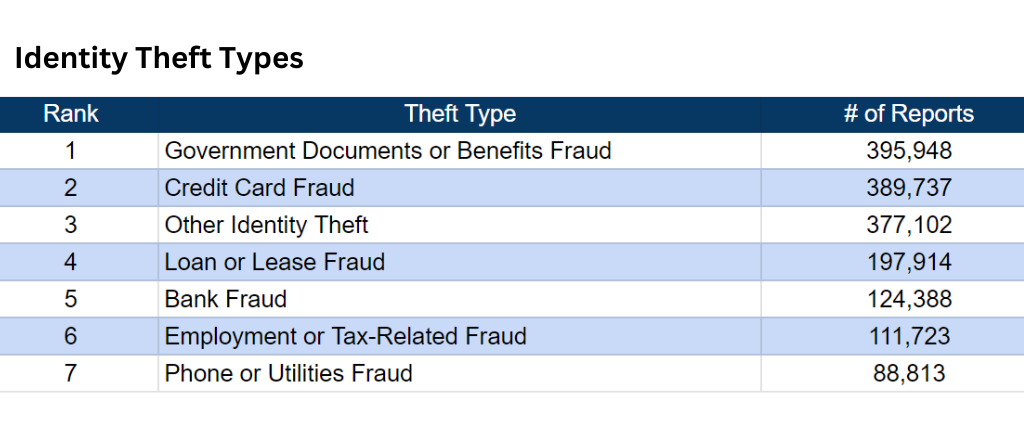

Document fraud is one of the identity theft frauds that tops all other identity frauds, according to the Consumer Sentinel Network Data Book 2021. The data suggests that 2021 reported the maximum number of government document or benefit fraud cases, accounting for 395,948 fraud reports, which only grows yearly.

This is especially critical in the dynamic lending landscape, where trust and accuracy are paramount.

Cybercriminals often target documents like tax returns, bank statements, government IDs, KYC documents, income statements, etc., to manipulate them or design a forged version for malicious purposes. As a lender, being responsible for these documents and minimizing fraud risks is essential to safeguarding your business and maintaining long-term customer trust and reputation.

This blog explores document fraud, its definition, challenges, different fraud detection methods, and how AI can prevent it.

What is document fraud in lending?

Document fraud is when cybercriminals duplicate, manipulate, counterfeit, or forge legitimate documents to access the systems or leverage financial gains.

This deliberate alteration or falsification of documents for fraudulent purposes helps fraudsters bypass legal checks and authorities. Here are some instances or examples of document fraud:

- Inflated income information on a forged income statement document is used to qualify for a loan, which otherwise wouldn’t make the borrower eligible.

- Altered identity documents, like passports or driving licenses, are used to impersonate legitimate users or borrow a loan under their name.

- Forged signatures on financial documents like promissory notes or loan agreements to obtain funds or commit identity fraud.

- Counterfeiting documents, such as insurance policies, to manipulate lenders into approving loans or extending credits.

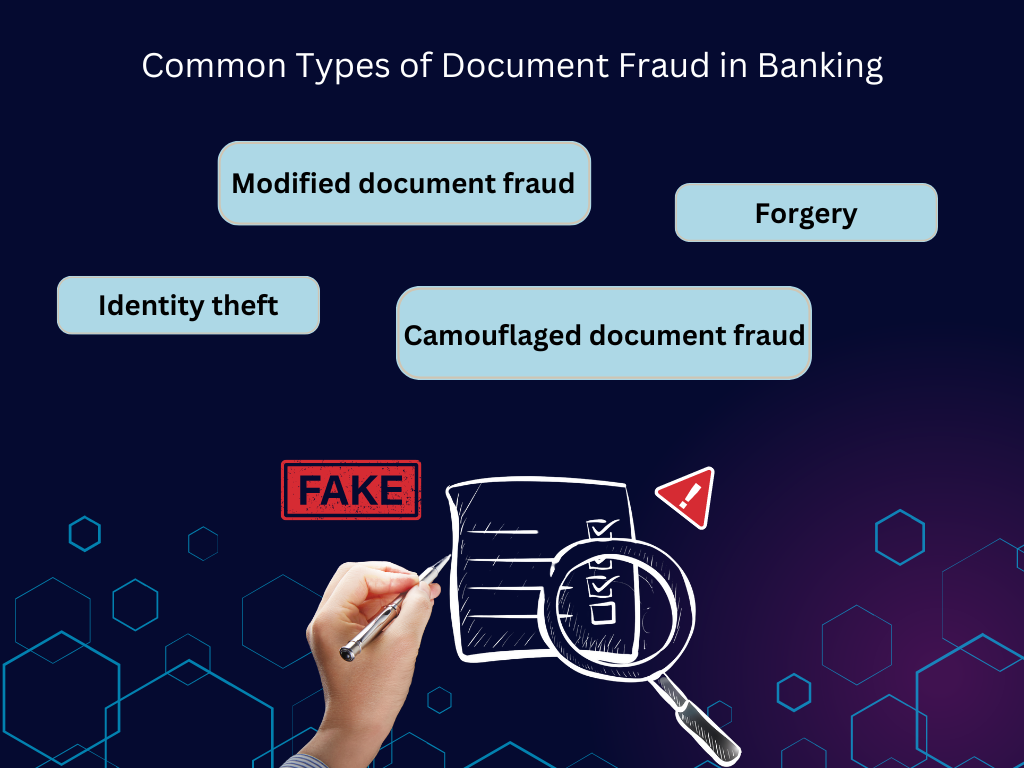

What are the common types of document fraud in banking?

Fraudsters incorporate several deceptive practices to commit document fraud with the intent to either steal someone’s identity, gain financial advantages, or harm a user’s reputation.

Here are the common types of document fraud fraudsters use in banking:

- Identity theft: This fraud occurs when fraudsters steal the complete identity along with the personal information, such as the social security number, name, or bank account details, of a user to apply for loans, create fraudulent accounts, or conduct unauthorized transactions.

- Forgery: Forgery in document fraud involves the fraudsters creating false documents with alterations, such as adding a forged signature or changing the user’s photo on identity documents to access funds or carry out unauthorized transactions.

- Modified document fraud: As the name suggests, modified document fraud involves fraudsters modifying or manipulating genuine documents. Fraudsters change details like the user’s name and address to trick lenders into approving a new credit line or for other financially malicious purposes.

- Camouflaged document fraud: In this document fraud, fraudsters create fake identities to represent themselves as authorized entities to gain financial advantage or access sensitive and highly confidential information.

Read more- Types of Fraud in Banking

What are Fraud Detection Systems?

Frauds are inevitable; hence, having a system in place that detects and prevents fraud in real time significantly helps minimize the risks and negative impact of fraud.

Fraud detection systems in banking and lending refer to software applications or platforms that help identify and prevent fraudulent activities. These systems typically operate in real time, continuously monitoring user activities, transactions, and other sources to detect anomalies or suspicious patterns.

Fraud detection systems aim to safeguard the critical data and integrity of lending operations by detecting fraud, such as document forgery, identity theft, and loan application fraud.

They use key features, such as anomaly detection, behavioral analysis, data integration, real-time monitoring and alerting, and machine learning, to flag fraudulent activities and prevent them from causing further financial and reputational damage.

As fraudsters and cybercriminals evolve and develop more sophisticated tactics, fraud detection systems must also evolve and leverage advanced algorithms and technologies to stay ahead of emerging threats and competition.

Types of Fraud Detection Systems

Fraud poses a significant threat to banks and financial institutions. Hence, employing robust technical approaches to fraud detection is essential to combat fraud. Here are the common types of fraud detection systems:

- Anomaly detection systems: These systems use machine learning algorithms and statistical analysis to identify anomalies or patterns that deviate from users’ normal behavior. By continuously comparing data with a pre-established user behavior baseline, anomaly detection helps easily detect fraudulent activities.

- Rule-based systems: As the name suggests, these systems use pre-determined rules or thresholds to flag suspicious or fraudulent activities based on specific conditions. For instance, a rule may be set to alert the system is a transaction if multiple login attempts occur at a time or if a transaction exceeds a certain amount.

- AI and ML-based systems: Artificial Intelligence or Machine Learning systems leverage advanced algorithms to analyze large datasets and learn from their trends or patterns to detect complex or subtle fraud patterns, which traditional rule-based systems can’t identify.

- Identity verification systems: These systems authenticate the user’s identity during login, account creation, or transaction initiation using methods like knowledge-based authentication, document verification, or biometric authentication to prevent risks of identity theft or account takeover.

- Network analysis systems: Network analysis systems examine the connection and relationship between different entities, such as users, transactions, and accounts, to detect fraudulent networks and prevent sophisticated fraud rings.

Traditional Approach vs AI Document Fraud Detection Systems

Here is a detailed comparison of traditional vs AI document fraud detection systems.

How do AI Fraud Detection Systems Work?

AI document fraud detection systems typically employ advanced Artificial Intelligence and Machine Learning algorithms to analyze multiple types of documents, like bank statements, identity cards, and contracts, to find fraudulent activities.

Here is the step-by-step process of how these fraud detection systems generally work:

- Document capture and preprocessing: The document fraud detection system first scans the documents using mobile devices and digital cameras to capture the documents’ high-resolution images. The captured document then goes through preprocessing, enhancing the document image quality and reducing noise.

- Text and feature extraction: The system then uses Optical Character Recognition (OCR) to extract text characters, symbols, and numbers as well as features, such as visual elements and metadata, from the scanned documents, which serve as inputs for the fraud detection models.

- Model training: The fraud detection AI model is then trained to learn patterns and user behavior based on historical data. This helps the system understand and distinguish normal behavior from suspicious or fraudulent activities.

- Fraud detection: Once the fraud detection model is trained, it analyzes the extracted documents’ features and data to identify signs of fraud by comparing the document characteristics against known fraud patterns and flag suspicious documents with anomalies and inconsistencies.

What are the benefits of using AI to fight fraud in lending?

Compared to traditional manual processes, using AI to combat fraud in lending offers several benefits to banks and businesses, including:

- Enhanced detection accuracy: AI and document fraud detection systems can easily analyze vast amounts of data efficiently and accurately, making detecting anomalies and patterns indicating fraudulent activities easier. This helps minimize false positives and enhance detection rates compared to traditional fraud detection.

- Real-time monitoring: Compared to traditional fraud detection systems, AI systems continuously monitor borrowers’ behavior and transactions in real time, ensuring instant fraud detection and identifying suspicious activities. This allows lenders to promptly prevent fraudulent loan requests from being approved.

- Adaptability: With fraudsters continuously evolving and adapting to new technologies, AI systems based on machine learning algorithms adapt to new fraud behavior and patterns by learning from the new data, allowing lenders to stay ahead of emerging fraudulent activities.

- Enhanced customer experience: By efficiently distinguishing between genuine and fraudulent documents, AI fraud detection reduces the risks of false positives, preventing inconvenient behavior for genuine borrowers and enhancing their overall experience.

- Cost reduction: Automating document fraud detection significantly reduces the labor costs required for intensive manual document checks and reviews. Furthermore, by reducing fraud risks, it also saves banks and lenders from fraud-related costs and expenses, enabling them to save a substantial amount of revenue.

- Scalability: With the growing lending operations and document investigations, AI fraud detection systems can easily scale and accommodate the expanding lending operations without compromising accuracy and efficiency.

- Regulatory compliance: AI-powered document fraud detection allows lenders to meet regulatory needs and compliance requirements, such as Anti-Money Laundering (AML) and Know Your Customer (KYC), preventing legal penalties.

Challenges in Implementing Fraud Detection Systems

While data security and protection processes have improved, fraudsters use advanced and sophisticated tools and technologies, such as social engineering, deepfakes, synthetic identities, and digital manipulation, to conduct fraud like document fraud.

Besides, they also mimic legitimate and genuine borrowers to conduct lending fraud, making it challenging for manual and traditional fraud detection systems to detect anomalies and identify fraud.

Here are a few more challenges banks and lenders face when implementing document fraud detection systems in their legacy processes:

- Lending operations involve a wide range and variety of documents, such as bank statements, passports, government-issued identity cards, and pay stubs with unique security features and identification requirements. This makes it challenging for legacy fraud detection systems to cover different types of documents when enabling fraud detection.

- Document fraud detection requires access to sensitive data, such as the borrowers’ driving license details, social security numbers, and financial statements. Ensuring data privacy and safeguarding this sensitive data against unauthorized breaches is essential which becomes difficult when dealing with document fraud detection systems manually.

- Integrating document fraud detection processes with existing lending platforms, verification processes, and customer databases can get complex and create challenges such as system interoperability, data synchronization, and compatibility issues, hindering efficient fraud detection.

- Adhering to regulatory compliance and requirements, such as AML and KYC, to legacy fraud detection systems can add complexity to the processes, making it difficult to identify and mitigate fraud risks.

- Lengthy and inconvenient verification processes without automation negatively impact borrowers’ user experience, leading to customer dissatisfaction.

Fight fraud with Arya AI Fraud Detection System

Combatting fraud against the evolving cybercriminal landscape need not be challenging, cumbersome, or expensive, and this is where Arya AI comes in.

At Arya AI, we offer an extensive range of APIs that help banks, businesses, and financial institutions significantly reduce fraud risks and ensure smooth business operations.

If you’re looking for efficient document fraud detection solutions, here are the key APIs we offer that you must look into:

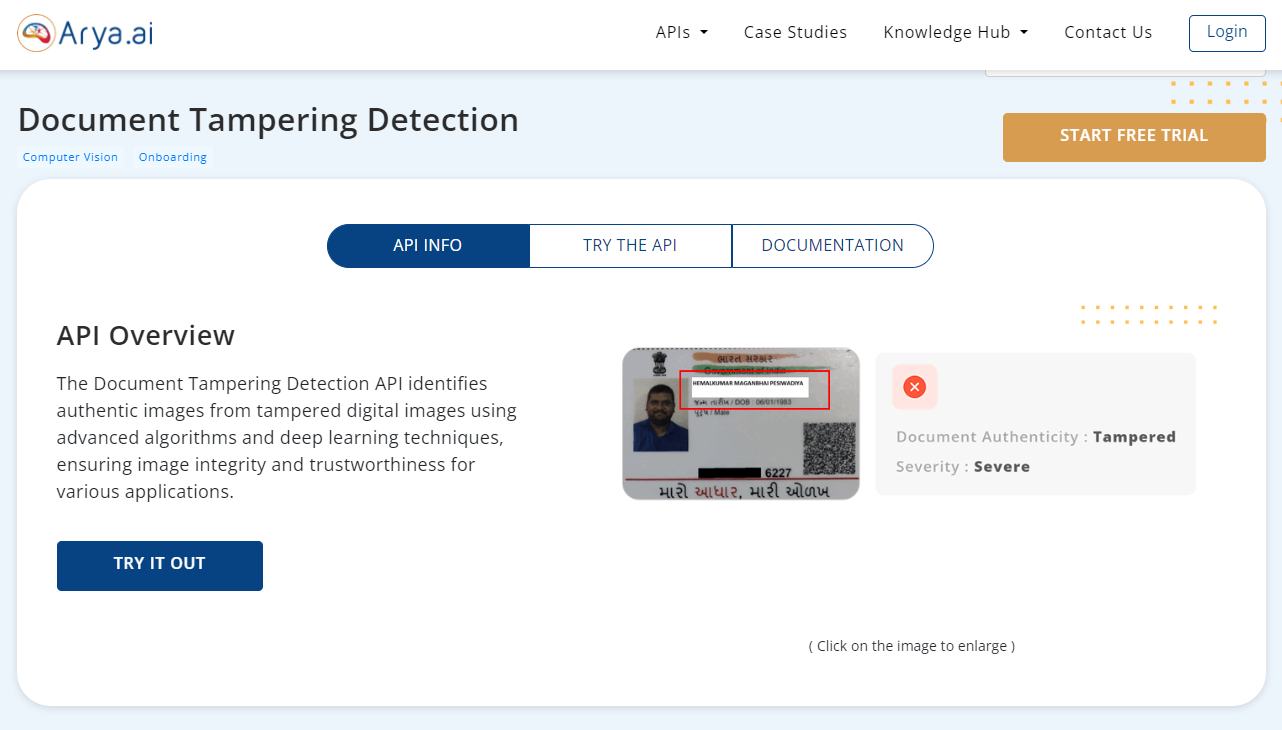

- Document tampering detection API accurately identifies authentic images of the scanned documents from tampered digital images to ensure integrity and trustworthiness.

- The KYC extraction API extracts information from several ID proofs, such as passports, PAN cards, and Aadhar cards, to enable smooth and frictionless eKYC verification of a user during onboarding and help banks meet KYC regulations.

- Bank statement analyser API reads the user’s transactional records and data from any bank to create comprehensive analytical reports containing important trends and suspicious anomalies, enabling efficient fraud detection.

- The signature detection API analyzes and detects multiple signature snippets from different forms and documents to return a confidence score of each detected signature snippet, preventing document fraud.

Besides these, we also offer several other critical APIs, such as deepfake detection, bank statement extraction, and invoice extraction. Click here to learn more.

Conclusion

Effective fraud detection systems are essential in combatting sophisticated fraud, maintaining the institutions’ trust and reputation, ensuring customer satisfaction, and avoiding financial losses.

With the increasing fraud risks, customer expectations, and regulatory requirements, relying on legacy manual document fraud detection isn’t the right choice. Instead, investing in AI-powered document fraud detection systems that enable real-time fraud detection is critical.

So, take a look at Arya AI’s cutting-edge solutions and APIs to stay ahead of the fraud and leverage scalable, flexible, adaptable, and affordable fraud detection solutions.

![A Comprehensive Guide to Document Classification [Challenges, Methods & Benefits]](/content/images/size/w960/2024/02/A-Comprehensive-Guide-to-Document-Classification.png)