Fraud in the banking sector is not new; it has existed since the formation of the first bank. Today, however, its scale and sophistication have reached unprecedented levels. With the quick digitization of the BFSI sector, fraudsters have found new ways to scam people, making fraud prevention in banks a dire need.

Nasdaq’s 2024 Global Financial Crimes Report describes financial crimes as a “multi-trillion dollar problem.” Both businesses and consumers have lost fortunes due to identity theft, credit and debit card fraud, and cyber-enabled scams.

As financial services become increasingly digital, the opportunities for fraudsters to exploit vulnerabilities are multiplying. This has made fraud prevention a critical focus for financial institutions worldwide. This blog will discuss the trends in banking fraud, everything that is needed in a fraud prevention framework, and how AI can help in fraud prevention in banks.

The Rising Threats of Banking Fraud

The types of fraud that banks face are varied and always evolving. Credit card fraud remains widespread, with unauthorized transactions leading to large financial damage. Identity theft is another major concern, where fraudsters use stolen personal information to open accounts or apply for loans.

Phishing schemes have grown more sophisticated, tricking individuals into revealing sensitive information through seemingly legitimate communications. Although less frequent, insider fraud poses a substantial threat due to the insider's access to critical systems and information.

Banks today face a multitude of fraud attempts, each requiring a vigilant defense. Here's a look at some of the most common threats:

Account Takeover (ATO): This prevalent fraud involves attackers gaining unauthorized access to a customer's bank account. Common tactics include stealing login credentials through phishing emails, SMS scams, or malware.

Payment Fraud:

- Card Fraud: Fraudulent use of credit or debit cards, including skimming (copying card data at ATMs) and counterfeit cards created from stolen data.

- Online Scams: Deceptive tactics like fake online stores or phishing emails that trick customers into revealing card details or making unauthorized payments.

New & Emerging Threats:

- Mobile Banking Malware: Malicious software specifically designed to steal login credentials or financial information from mobile banking apps.

- Social Engineering: Psychological manipulation tactics used to trick victims into divulging personal or financial information. This can involve impersonating bank officials, calling with urgent requests, or creating fake social media profiles to gain trust.

Read more- Types of Fraud in Banking

Emerging Trends in Banking Fraud:

One particularly troubling trend is Synthetic Identity Fraud. This involves creating fake identities by mixing real and fake information. These synthetic identities can slip past traditional verification systems, allowing fraudsters to open credit accounts, secure loans, and ultimately leave banks with substantial losses when they vanish without a trace.

Account Takeover Fraud is also on the rise. As mentioned earlier, this type of fraud involves cybercriminals using stolen credentials. Once they have control, they can siphon funds, make purchases, and even conduct more fraudulent activities within the account, often going unnoticed until significant damage is done.

Cyber attacks, including ransomware and Advanced Persistent Threats (APTs), have become more targeted and sophisticated. Banks, holding vast amounts of valuable data, are prime targets. These attacks can paralyze banking operations, leading to severe financial and reputational damage.

The proliferation of mobile banking has introduced new vulnerabilities, as fraudsters exploit weaknesses in mobile security to access accounts and execute fraudulent transactions.

What is Fraud Prevention in Banking?

Fraud prevention in banking is a complete set of strategies and measures incorporated into the workflow of financial institutions to defend customer accounts, transactions, and data from unauthorized access and fraudulent activity. The primary goals are:

- Protecting Customer Funds: This is paramount. Effective fraud prevention in banks nullifies the risk of customers losing their hard-earned money through unauthorized transactions or account takeover.

- Maintaining Customer Trust: When customers feel their money is secure, they are more likely to maintain a positive relationship with the bank and use more of its other services. Otherwise, they’re only likely to stick with basic banking services. A data breach or fraud incident can severely damage customer trust, leading to bank account closures and reputational harm.

- Ensuring Regulatory Compliance: All governments impose various regulations on financial institutions to protect consumers and prevent money laundering. Banks' robust fraud prevention demonstrates their commitment to compliance and mitigating potential regulatory fines.

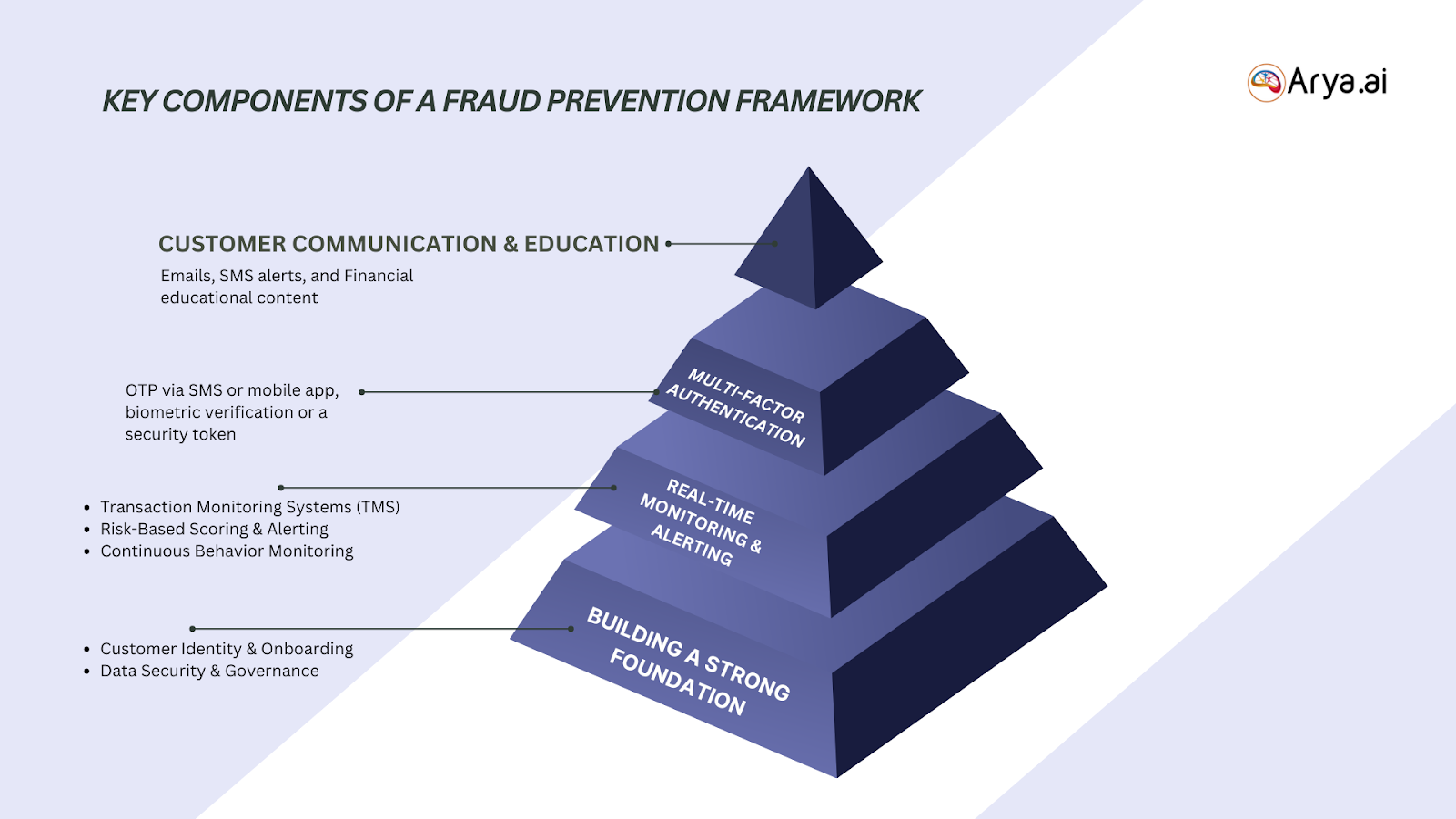

Key Components of a Comprehensive Fraud Prevention Framework

Building a powerful guard against fraud, especially in banking, requires a multi-layered approach. Here are some key components of a comprehensive fraud prevention framework:

Building a Strong Foundation:

- Customer Identity & Onboarding: The fight against fraud starts at account opening. Implementing strong customer identity verification processes is crucial. This includes verifying identity documents, using reliable data sources, and potentially employing additional checks for high-risk accounts. KYC Extraction modules and powerful Document Tampering Detection APIs can help during these processes.

- Data Security & Governance: Customer data is a goldmine for fraudsters. Robust data security practices, such as encryption, access controls, and regular security audits, are essential to protect sensitive information.

Real-Time Monitoring & Alerting:

- Transaction Monitoring Systems (TMS): These systems continuously monitor transaction activity for suspicious patterns. TMS analyzes factors like transaction size, location, merchant type, and spending habits to identify anomalies that might indicate fraud.

- Risk-Based Scoring & Alerting: Banks can leverage risk-scoring models that assign a risk score to each transaction based on various factors. High-risk transactions trigger alerts for further investigation or potential blocking.

- Continuous Behavior Monitoring: Customer behavior analysis goes beyond individual transactions. Monitoring a customer's banking activity over time can reveal unusual patterns indicative of potential account takeover attempts. Big Data Modelling platforms can handle such vast amounts of data from customers.

Multi-Factor Authentication (MFA):

MFA adds a layer of security to the login process by requiring a second factor beyond just a username and password. This could be a one-time password (OTP) sent via SMS or mobile app, biometric verification like fingerprint scanning, or a security token. MFA significantly increases the difficulty for unauthorized individuals in gaining access to accounts.

Customer Communication & Education:

- Importance of Customer Awareness: An informed customer is a powerful ally in fraud prevention, so banks are responsible for educating customers about common fraud tactics and how to report suspicious activity.

- Strategies for Educating Customers: Employing multiple communication channels like emails, SMS alerts, and educational content on the bank's website or mobile app can raise awareness. Regular phishing simulations can also help customers identify and avoid scams.

The Role of AI in Fraud Prevention for Banks

AI has become a game-changer in the fight against fraud for banks. With complex machine learning algorithms, banks can analyze vast amounts of data, identify subtle patterns, and predict future threats with an accuracy that surpasses traditional methods. Here's a look at some of the key roles AI plays in fraud prevention for banks:

- Machine Learning for Anomaly Detection: As mentioned earlier, AI identifies anomalies in transaction data. Machine learning algorithms can analyze factors like transaction size, location, merchant type, time of day, and historical spending habits to flag suspicious activity that might go unnoticed by traditional rules-based systems.

- Predictive Analytics for Proactive Defense: Predictive analytics models can analyze historical fraud data and identify patterns or trends associated with fraudulent activity. This means that banks can take preventive measures, such as implementing stricter authentication for high-risk transactions or blocking suspicious login attempts before they occur.

- Enhanced Risk Assessment & Decision Making: Risk scoring models are a cornerstone of fraud prevention in banks, and AI significantly improves them. AI risk management models can incorporate more data points, including customer demographics, device characteristics, behavioral patterns, and external threat intelligence. This allows for more accurate risk assessments, helping banks to better differentiate between legitimate and fraudulent transactions.

- Network Analysis & Social Network Detection: AI can analyze transaction networks to identify suspicious connections between accounts or entities. This can help uncover fraud rings or money laundering schemes. Social network analysis can also be used to identify fake accounts or stolen identities by examining connections and interactions between accounts.

- Customer Segmentation & Behavior Profiling: AI can be used to segment customers based on risk profiles and behavior patterns. This allows banks to customize their fraud prevention strategies to specific customer groups. For example, high-risk customers might require stricter authentication measures, while low-risk customers can enjoy a more frictionless experience.

Challenges in Implementing AI Fraud Prevention in Banks

If AI models are the best way to prevent fraud in banks, why aren’t they already implemented in all banks? This is because implementing it comes with its own set of challenges:

Data Silos & Integration Challenges:

Often, valuable data resides in disparate banking systems, preventing you from having a full view of customer activity. Fragmented data makes it difficult for AI models to analyze all relevant information for better fraud detection.

- Solution: Build a centralized data platform or adopt a data lake architecture. This allows for data consolidation from various sources, giving AI algorithms a comprehensive view of customer behavior and transactions.

Balancing Security & Customer Experience:

It is not easy to strike the right balance between robust security and a seamless customer experience. Overly stringent security measures can frustrate genuine customers, leading to cart abandonment or account closures.

- Solution: Adaptive authentication offers a way to address this challenge. This approach uses risk-based factors mentioned earlier to find the level of authentication needed for each transaction. Trusted users with a low-risk profile can have a frictionless login process, while high-risk scenarios might trigger additional authentication steps, such as MFA, to ensure security.

Staying Ahead of Evolving Threats:

Fraudsters are continuously innovating and developing new tactics to bypass security measures. A static fraud prevention system becomes vulnerable over time.

- Solution: The key lies in deploying a flexible and scalable AI-powered framework. While all machine learning algorithms can continuously learn, the right feedback and data need to be provided to help them adapt to new fraud patterns and emerging threats.

Fraud Prevention with Arya AI

In today's dynamic banking environment, preventing fraud in banks requires a powerful and adaptable defense strategy. Arya AI offers an AI-powered API suite for fraud prevention in banks.

Alongside essential tools like the Bank Statement Analyser, Signature Detection, and Cheque Extraction, which ensure the integrity of financial transactions, Arya AI extends its capabilities to encompass Identity Verification. This system is designed to help financial institutions proactively combat fraud and safeguard their customers.

Addressing the Challenges of Fraud Prevention in Banks:

Arya AI's solutions directly address the challenges mentioned previously:

- Centralized Data Platform: Arya AI's platform eliminates data silos by consolidating data from various banking systems. This provides a holistic view of customer activity for the best fraud detection.

- Fraud and Anomaly detection: Analyze real-time data and identify suspicious patterns with Arya AI. This proactive approach enhances security, reduces fraudulent activities, and ensures the integrity of your financial operations.

- Risk-Based Authentication: Arya AI’s solutions incorporate risk-based authentication, ensuring a balance between security and customer experience. Trusted users can experience a frictionless login process, while high-risk scenarios trigger additional authentication steps.

Advantages of Using Arya API Suite

Arya AI’s AI-powered fraud prevention solutions offer several key benefits for banks:

- Reduced Fraud Losses: Arya AI helps banks minimize financial losses by proactively identifying and preventing fraud attempts.

- Improved Customer Experience: Arya AI’s solutions ensure a seamless and frictionless banking experience for legitimate customers.

- Enhanced Regulatory Compliance: Robust fraud prevention measures help banks comply with relevant regulations and avoid potential fines.

With Arya AI, financial institutions can gain a significant edge in the fight against fraud. By leveraging the power of AI and machine learning, Arya AI empowers banks to protect their customers, streamline operations, and build trust.

Conclusion

In this digital era, where anyone can easily and freely access the latest advancements in AI, a comprehensive fraud prevention framework is necessary. As fraudsters employ increasingly sophisticated tactics, banks require a robust defense strategy to safeguard customer funds and maintain trust.

Banks can gain a significant advantage in fraud prevention by leveraging AI-powered solutions like those offered by Arya AI. Arya AI's comprehensive suite of solutions addresses key challenges like data silos, provides real-time transaction monitoring, and implements risk-based authentication for a seamless customer experience. Are you ready to build a future-proof fraud prevention framework and protect your customers? Contact Arya AI to know more about how our solutions can empower your bank to stay ahead of evolving threats and ensure a secure banking experience.